2021 Second Quarter Market Commentary: Play Ball

Commentary

Play Ball

What a welcome sight to see fans back in the ballparks cheering their respective teams in person rather than virtually. After a year of lockdowns, the broader economic reopening has also been welcomed by the equity markets. The S&P 500 kept rounding the bases in the second quarter, rising over 8% for the quarter to all-time highs, fueled by the prospects of stronger economic data. Given that markets tend to quickly discount new information, the summer months are likely to produce a range bound tug of war in equities between improved fundamentals and uncertainty around interest rates and inflation. So, while investors should not be surprised by a seventh inning stretch over the near-term, we continue to believe this market has a lot of game left to play over the long-term.

The Good

When evaluating today’s investment landscape, the old western movie title “The Good, the Bad and the Ugly” comes to mind. Though a more apropos categorization of current events is closer to ‘The Good, the Still Improving and the Worth Watching’. First the ‘Good’. The monetary and fiscal stimulus employed early in the pandemic and later combined with the vaccine development have successfully gotten the economy across the COVID-chasm and to the starting line of a return to normal. Businesses are reopening, employees are returning to offices and consumers are once again venturing out to malls, restaurants and sporting events. All this has set the stage for a much larger than average expansion of GDP in 2021 that is expected to carry on into next year as well. Additionally, corporate earnings are likely to surprise to the upside as analyst estimates made at the nadir of the pandemic prove overly pessimistic.

The Still Improving

Within the ‘Still Improving’ category, a couple of dynamics stand out. A year’s worth of pent-up demand for all manner of goods and services has overwhelmed producers and supply chains creating numerous dislocations that will take time to balance. Businesses are reopening to eager customers creating a huge need for workers. This is clearly evident in ‘Help Wanted’ signs in just about every storefront. The high-volume strategy of a local distributor of metals and industrial supplies has been my personal favorite. It certainly did its job of catching my attention during my commute.

We anticipate that laborers will increasingly head back to work as vaccinations rise, employers offer incentives and government programs wind down. And while wages across many entry-level positions have risen of late and deservedly so, a growing labor force will help keep wages from spiraling to the point of economic harm. Inventories of physical goods are also running well below current demand levels. Buying a bike has never been such a challenge! We expect this imbalance to ebb as well as manufacturers get operations back to full capacity and higher prices in the most affected areas temper demand until inventories can be fully replenished.

The Worth Watching

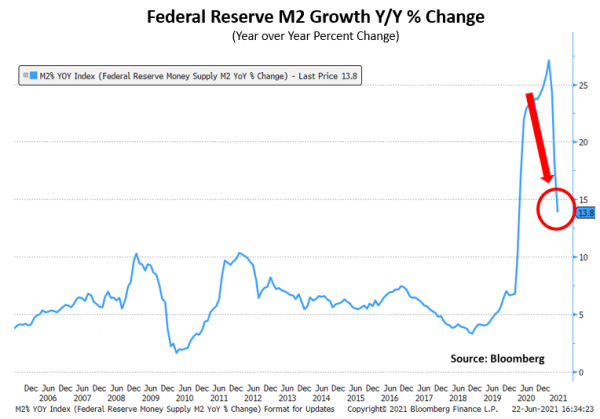

Lastly, we arrive at the ‘Worth Watching’ segment where inflation is far and away the headliner. The inflation debate centers around whether the recent rise in prices will be transitory in nature or turn into a longer-term, structural headwind for consumers and investors alike. One cannot ignore the absolute rise in the M2 money supply (a closely watched indicator of future inflation) whose ascent the past year was driven by increased savings during the lockdown along with multiple injections of federal stimulus checks. What is missed however, is that the pace of growth of the M2 money supply (which includes cash, checking and short-term deposits) has already begun to ease significantly with the wind down of government stimulus and the reopening of the economy as consumers can get out and spend again as seen in the chart below.

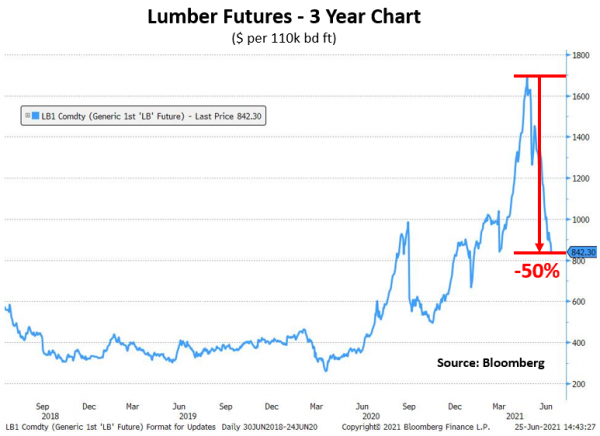

A further example of easing pressure can be observed via the recent movement in lumber prices. Last year, as lumber mills went offline, suppliers were caught off guard by rising demand as consumers abandoned vacation plans and instead turned to home improvement projects which caused prices to rise dramatically. As the chart here shows however, as these imbalances trend towards equilibrium, prices can come down just as fast as they rose. Lumber prices have fallen 50% since peaking just a few short months ago.

Overall, inflation anxieties are likely to recede with the stabilization of the money supply and as the majority of recent price hikes follow a path similar to that of lumber. That said, a little inflation is healthy, but we certainly want to avoid sustained higher price levels. Going forward, we will continue to watch for expanded and persistent upward wage pressures as the ultimate canary in the inflation coal mine.

Human behavior tends to extrapolate the most recent past into perpetuity. It is important as long-term investors to not lose the forest for the trees recognizing there will always be uncertainties within the market. After the volatility of the past year, it will no doubt take time for market imbalances to work through the system. And there will likely be bumps along the way as seen through the price moves of many goods and services. As for us, we will grab our box of Cracker Jacks and enjoy watching an economy whose GDP and earnings are poised to surprise over the remainder of the year.

As always, thank you for reading and please do not hesitate to reach out to us if we can assist you with your investment goals in any way.

Kindest Regards,

Jeffrey B. Travis, CFA

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell.

This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC. Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.