2021 Fourth Quarter Market Commentary: Phase 3 of the Pandemic Market

Commentary

2021 Fourth Quarter Market Commentary & 2022 Outlook

Phase Three of The Pandemic Market

The US stock market gained 11% in the fourth quarter of 2021 as the road to economic normalcy continued to lift equities despite the emergence of a new Covid variant. For most of the past year, simulative fiscal policy and loose monetary conditions combined to create a robust environment for stocks. While the investment backdrop in 2022 may prove more opaque, the fact the outlook isn’t perfectly rosy may actually benefit equities. The emergence of Omicron may induce concern, but the stock market has proven its ability to look beyond case counts. In 2022, if the pandemic’s hold on the world continues to ease, a more synchronized recovery may develop, as vaccine proliferation and immunity levels allow global economies to reopen.

Thus far, the US market’s performance during the Coronavirus pandemic can be broken down into two distinct phases. The first phase, lasting 6 months from March to October 2020, was characterized by the initial correction, the restrictions to “flatten the curve”, and the economic uncertainty that followed. The second phase, which included much of the past 15 months, commenced once trials for a Covid vaccine indicated a safe and effective inoculation was forthcoming and the threat of economically restrictive measures were eliminated. As a result, over the past year, the S&P 500 Index rose 28.7% with consumer spending rebounding strongly.

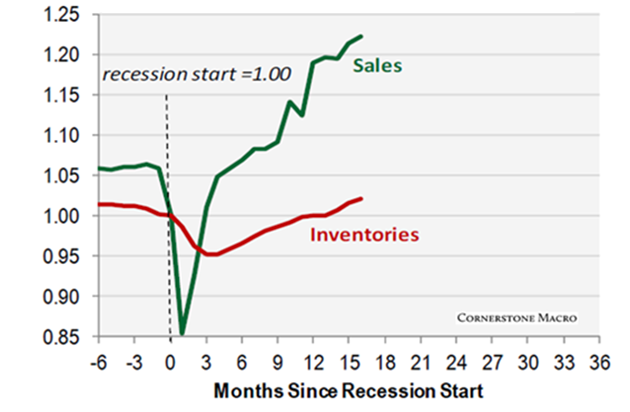

During the year, the combination of flush consumers and disrupted supply chains has resulted in widespread inflationary pressures. In November 2021, the year-over-year change in the popular measure of inflation, the Consumer Price Index, jumped 6.8%; the largest spike in 30 years. It is a textbook example of too much money chasing too few goods. The adjacent chart represents the core problem. At this stage of a recovery, sales have recovered but the inventory replenishment remains hampered by the pandemic. This isn’t too surprising as it is easy to downsize but more time consuming to rehire, restart and retrain.

Manufacturing, Wholesale & Retail Sales & Inventories

For consumers, prices for groceries, gasoline, rent, etc. are all up. Whether the resulting inflation is temporary or persistent is still undetermined, but most likely depends on the end products input costs. Industries exposed to more commodity-driven inflation can adjust quickly once production and raw materials inventories recover. For service industries, the impacts of wage inflation may persist.

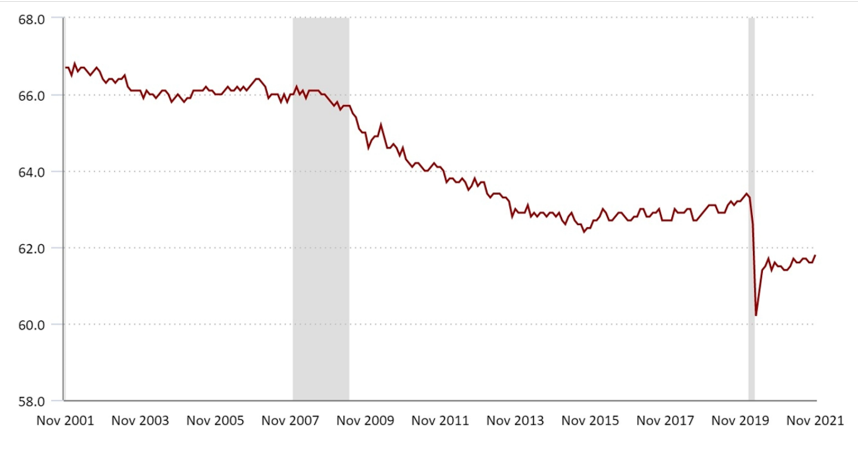

Exacerbating the underlying inflation pressures is a tight labor market. Although the unemployment rate has fallen sharply from its pandemic peak to 4.2% in the fourth quarter of 2021, this statistic downplays the reduction in the overall workforce from individuals that left the labor market for one reason or another. Whether tempted by early retirement, to gig work opportunities, or into starting a home-based business, the labor pool contracted during the pandemic. The result is a historically wide disparity between the number of available workers and job openings, highlighting the competitive and challenging labor market.

US Civilian Labor Force Participation Rate (SA)

Source: US Bureau of Labor Statistics

2022– Phase 3

The outlook for 2022 is cloudier than in 2021, as the risks of inflation, high valuations, and the Federal Reserve’s response bear consideration. The Fed will be the largest wildcard next year as it contemplates action to address inflation and follow through on its intent to rescind the massive injection of monetary liquidity. Yet the risks from supply constraints, labor shortages, and Covid variants might keep the Fed reluctant to act too aggressively. The market is poised to confront Phase 3 of the pandemic market, the gradual withdrawal of external financial support.

A reduction in the Fed’s bond buying has already been revealed and this could hamper asset prices as the proverbial floor is removed. Previous attempts to end quantitative easing have been somewhat futile and eventually revoked. When the Fed stopped expanding its balance sheet between 2015 and 2017 in an effort to withdrawal the support provided following the sub-prime crisis, the market initially reacted negatively and treaded water, but the S&P 500 still managed to rise 38% during the 3-year pause. So, while it is unnerving to have the support removed, stocks can still advance as policy is unwound.

In periods of inflation, stocks have also been a good place to reside, as revenues and earnings rise. To combat persistent inflation, the Fed could hike rates even if only to remind market participants it will use all tools at its disposal. Debate over when the Fed could start its rate increase cycle and how aggressively will likely periodically rattle stocks. Yet, even if short-term rates rise from suppressed levels, it typically takes several quarters before a tightening cycle slows growth and hampers profits. Current supply chain disruptions and labor shortages are also natural breaks on the economy that could keep the Fed sidelined. Certainly, rate hikes bear watching, but their impact is more likely a 2023 risk for equities. Until then, the stock market will look past Omicron and “climb the wall of worry”.

As we move into 2022, Phase 3 of the pandemic market will see the slow walk-back of external supports and stimulus. We continue to favor companies with the ability to grow earnings and market share regardless of the economy’s growth rate. At this stage of the market cycle, high-quality (and highly profitable) companies are always preferable to distressed assets, even though the latter can offer phenomenal returns periodically. But while the cyclical recovery lifted all boats early in Phase Two of the pandemic market, that rising tide has crested and we believe financial strength, a respect for shareholder capital, earnings growth and valuation will determine long-term investing outcomes. Companies that can grow through innovation and productivity, independent of the rate of GDP, remain our preferred investments.

Tk you for reading.

Robert Stimpson, CFA, CMT

Co-Chief Investment Officer & Portfolio Manager

Oak Associates, ltd.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell.

To determine if this Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund’s Prospectus which may be obtained by calling 1-888-462-5386 or visiting our website at www.oakfunds.com. Please read it carefully before investing. Mutual fund investing involves risk, including possible loss of principal.

This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC. Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

Ultimus Fund Solutions, LLC is not affiliated with Constant Contact.