2019 Fourth Quarter Market Commentary: Monsters Under the Bed

Commentary

Monsters Under the Bed

January 2, 2020

The past year was a phenomenal period for US equities. The S&P 500 rose 31.4% in 2019, fueled by falling interest rates thanks to the Federal Reserve (the “Fed”). Growth stocks drove popular benchmarks higher, with outsized gains in some of the largest companies in the economy. Strength appeared broad based, but internal metrics were mixed, which may highlight areas of opportunity going forward.

Admittedly, overall performance in 2019 was somewhat unusual. Defensive and stable sectors rose as much, if not more, than “growthier” cyclical sectors. Apart from Healthcare, other traditionally defensive sectors such as Utilities, Telecom, and Staples, were up 26%, 32%, and 27%, respectively. Technology stocks within the S&P 500 were the standout performers, gaining 50%. Healthcare stocks, however, suffered a perfect storm of negative sentiment, congressional oversight, and increased risks associated with the opioid epidemic. The group rose 20% but its underperformance has increased the attractiveness of the Healthcare sector in our opinion. Energy stocks were the worst group in 2019, rising only 11%.

Super-Sized

An interesting aspect of 2019’s performance was the strong return of the largest companies in the benchmark index. Size is usually a limitation to long-term performance. Yet Apple rose 88% in 2019 and Microsoft gained 57%. These outsized returns of the two largest companies in the major indexes skewed the performance of popular benchmarks. When size is ignored in performance, the S&P 500 Equal Weighted Index lagged the market cap-weighted index by over 2.5%.

Whether or not the largest of the large, which happen to also be amongst the biggest winners of the past decade, are able to retain their top 5 position over the next decade may prove difficult. They will each need to innovate and develop new market opportunities. Ten years ago, few could have predicted that PC makers Microsoft and Apple would need to become leaders in cloud computing, cellphones, mobile apps, wearables, and gaming to retain their dominate positions. Even Amazon, once viewed as the Wal-Mart of the internet, has become a major player in web-services, streaming content, and smart devices. We are excited for what the future holds and are hesitant to punish past results, innovations, and size.

Looking Forward

That said, looking into 2020 we are often asked about what keeps us up at night. Predicting a recession is often simple folly, and changing portfolios prematurely is dangerous. If investors had heeded the bond market’s “recession warning” when the yield curve first inverted in March 2019, they would have missed out on a 17% run in US equities (as seen by the S&P 500). Yet, we need to be realistic that 20%+ equity market returns are hard to sustain if economic data falters. So what are the monsters under the bed that keep us up at night?

Boogieman #1 – The Fed

Most remember the terrible quarter US equities experienced in Q4 2018. The 14% quarterly drop in the S&P 500 occurred after the Fed, which had been raising interest rates, signaled it felt the neutral rate, or level that was neither stimulative nor restrictive to the economy, was still a ways off. Fear that the Fed would persist in raising interest rates to a level market participants felt was too high and thus produce a recession, crushed stocks. Fortunately, economic data (such as leading economic indicators) didn’t forecast a recession and the market recovered. A pivot from the Fed, which eventually clarified that it would reconsider its target expectations, also helped calm the market.

Nevertheless, we continue to believe the Federal Reserve’s long-term goal is to raise interest rates to a level that would re-arm its monetary policy tool kit. With the current economic expansion more than 10-years in length without suffering a true recession, the Fed will want to be as equipped as possible to deal with one if necessary. It also knows that sustained low-interest rate environments can produce excesses that can end very painfully. Think bubbles driven by cheap money, such as housing, sub-prime debt, and energy exploration.

Should the Fed return to its mission of higher interest rates, accompanied by rhetoric to soften the impact of their intent, stocks could experience a sustained correction. Fortunately, with the 2020 presidential election forthcoming, the Fed will be cautious to intervene, positively or negatively in the economy, unless absolutely necessary.

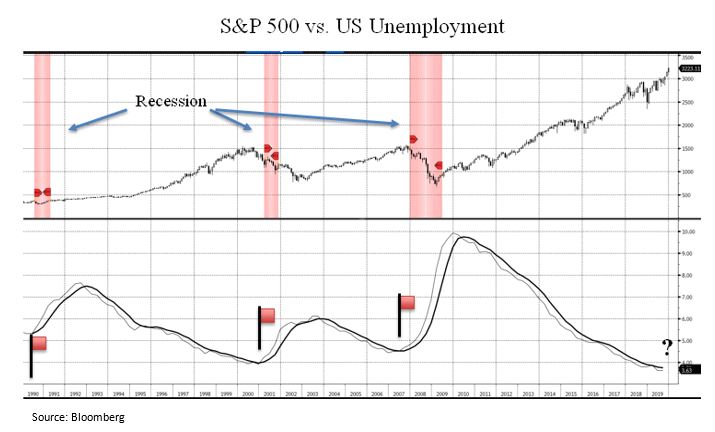

Boogieman #2 – Unemployment

An important early warning sign of a recession is a change in trend in the unemployment rate. This has been discussed several times in past market commentaries, so I’ll keep this short. Unlike other leading economic indicators, a pickup in unemployment has reverberations across the economy. When companies cut jobs to protect their profit margins and earnings, it creates ripples that directly affect consumer spending, consumer confidence, housing prices, and loan delinquencies.

Changes in the unemployment rate highlight the end of economic expansions better than signaling a recovery, as hiring often lags. So while the trend in employment has been strong for the past decade with the unemployment rate falling to a 50 year low of 3.6%, it remains a monster we vigilantly watch for anything more than slight fluctuations.

The chart below from Cornerstone Macro details the performance of Financials during the 2008-2009 sub-prime crisis. It notes the nearly dozen governmental actions taken to solve the crisis before stocks were able to find a bottom. While the market has responded positively to the recent stimulus package, the economic pain may not yet be fully understood and further supportive actions may be required. The US stock market may therefore struggle to return to pre-Covid levels while still facing months of terrible earnings report, the realities of the economic destruction caused by the pandemic, and potential flare-ups of the virus once quarantines are loosened. Unlike prior stock market corrections, this one is not driven by a fragility within the financial system, but by an unprecedented health care crisis.

The Tortoise and the Hare

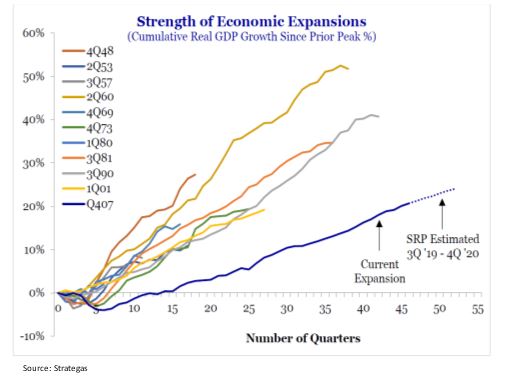

The economic expansion that has lasted this decade was notable for two things. Not only was it one of the longest on record, but it was also one of the slowest. Slow and steady has won the race. With inflation absent and interest rates low, equities have enjoyed a slow growth environment that sent the S&P 500 up 250% since year end 2009. Going forward, we expect the current low growth, low interest rate environment to continue to benefit equities. A pickup in international economies could also add an additional leg to the current expansion.

While a recession will eventually appear, predicting one prematurely can also be financially devastating. We expect the current low inflation, slow growth environment to persist. Thus the outlook for US equities remains favorable. We remain cautiously optimistic with one eye on the monsters under the bed.

Thank you for reading and Happy New Year.

Robert Stimpson, CFA, CMT

Co-Chief Investment Officer & Portfolio Manager

Oak Associates, ltd.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell.

To determine if this Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund’s Prospectus which may be obtained by calling 1-888-462-5386 or visiting our website at www.oakfunds.com. Please read it carefully before investing. Mutual fund investing involves risk, including possible loss of principal.

This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC. Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

Ultimus Fund Solutions, LLC is not affiliated with Constant Contact.