Insights

Oak Associates Named to PSN Top Guns List of Best Performing Strategies for 4Q 2025

Quarterly PSN Top Guns List published by Zephyr identifies best-in-class separate accounts, managed accounts, and managed ETF strategies.

Akron, OH—February 18, 2026— Oak Associates announced today it has been named to the celebrated PSN Top Guns List of best performing separate accounts, managed accounts, and managed ETF strategies for Q4 2025. The highly anticipated list, published by Zephyr, remains one of the most important references for investors and asset managers.

“These managers have successfully steered through transformative events such as the COVID-19 pandemic market crash, the Brexit referendum, the US-China trade war, the global sell-off of 2015-2016, and the AI-Driven market this year”, says PSN Product Manager Nick Williams. “Their ability to adapt to evolving market conditions, strategically position across asset classes, and capture opportunities underscores the enduring importance of active management in delivering value to investors.”

Oak Associates Technology Select is a sector-specific strategy that seeks long-term capital growth by investing primarily in large-capitalization stocks of companies whose earnings and sales growth are driven by technology-related products and services. The investment process involves identifying the most attractive areas within technology and narrowing the search to individual stocks. The portfolio managers generally prefer market leaders with strong fundamentals that are trading at attractive valuations and have also shown a commitment to returning capital to shareholders.

“Being named a PSN Top Guns Manager of the Decade is a tremendous honor that validates our investment team’s disciplined approach. We’re proud that our long-term focus on identifying innovative market leaders and maintaining a consistent approach has delivered strong results for our clients,” said Oak Associates’ Portfolio Manager, Jeff Travis.

Through a combination of PSN’s proprietary performance screens, the PSN Top Guns awards products in six proprietary categories in over 75 universes based on continued performance over time.

Oak Associates’ Technology Select strategy earned a PSN Top Guns Manager of the Decade award, meaning our Technology Select strategy had an r-squared of 0.80 or greater relative to the style benchmark for the latest 10-year period. Moreover, the strategy’s returns were greater than the style benchmark for the latest 10-year period and had a standard deviation less than the style benchmark for the latest ten-year period. At this point, the top ten performers for the latest 10-year period become the PSN Top Guns Manager of the Decade.

The complete list of PSN Top Guns and an overview of the methodology can be located at https://psn.fi.informais.com/PSNTopGuns/topguns_zephyr.asp

Oak Associates is an investment management firm located in Akron, Ohio. Founded in 1985, Oak has spent decades focused on U.S equities and uncovering quality growth companies that can rise above market expectations. At Oak, we believe that sustainable long-term growth for investors is best achieved through a concentrated focus on companies and sectors. Our high-conviction stock selection process centers on identifying multiple drivers of growth and engaging in fundamental research to uncover the right businesses within the right sectors. We then take meaningful positions—targeting unrealized value and seeking long-term capital appreciation independent of typical index results. We offer two key ways to invest with us, including mutual fund accounts and direct separate accounts for institutions and high net worth individuals.

For more than four decades, PSN has been a top resource for investment professionals. Asset managers rely on Zephyr’s PSN to effectively reach institutional and retail investors. Over 2,800 firms, 285 universes, and more than 21,000 products comprise the PSN SMA database showing asset breakdowns, compliance, key personnel, ownership diversity, ESG, business objectives and strategy, style, fees, GIC sectors, fixed income ranges and full holdings. Unique to PSN is its robust historical database of over 40 Years of Data Including Net and Gross-of-Fee Returns. Zephyr’s PSN produces the PSN Outlook eBook series provides insight and trends about the SMA industry. You can view them online here.

Visit PSN online to learn more.

No compensation was directly or indirectly provided by the Adviser in connection with this rating and/or award.

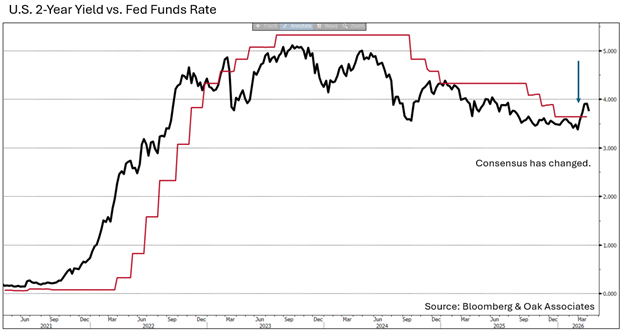

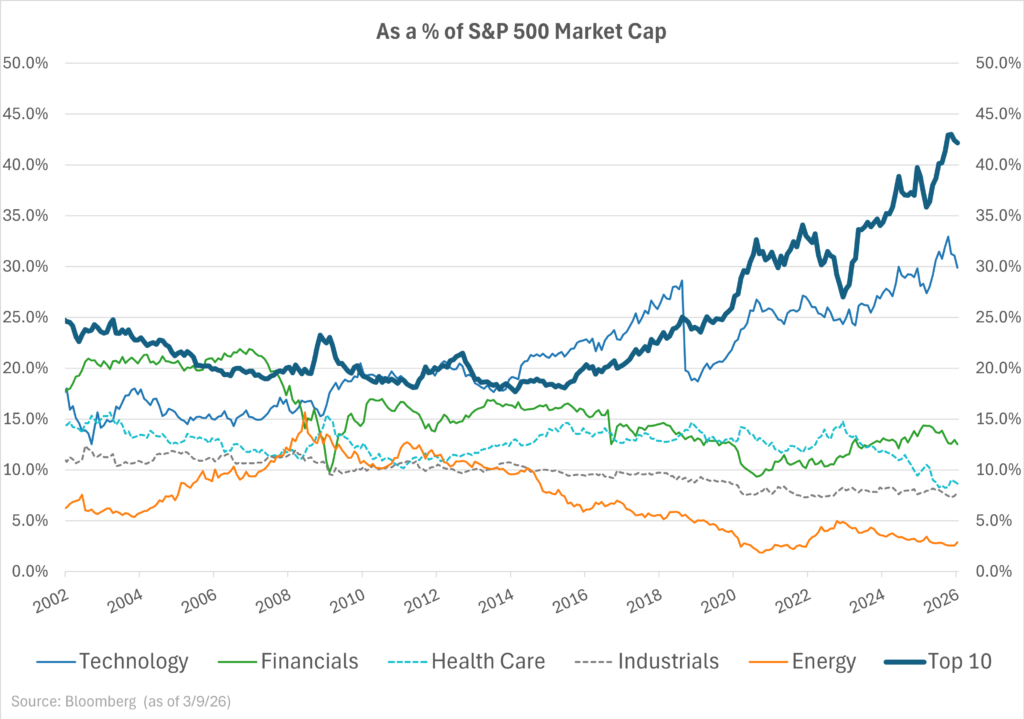

In recent years, equity markets have undergone significant changes, marked by rising market concentration, particularly within large-cap U.S. technology stocks. Almost 35% of the U.S. stock market’s current value is concentrated in companies known as the “Magnificent 7” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla), with the performance of these companies accounting for 42% of total market returns in 20251 and momentum a key element of the Magnificent 7 tech stocks driving outsized returns since 2022. Indeed, U.S. stock market concentration in 2025 surpassed its previous peak of 1932.2 As also seen in the Market Cap graph illustration of the top 10 holdings of the S&P 500, this elevated concentration introduces unexpected risks for investments that passively mirror a benchmark.

When a disproportionate share of market performance and investor capital is tied to a handful of dominant stocks, portfolio vulnerability increases within passive investment structures not designed for higher concentration holdings. Shifts in market sentiment, regulatory changes or unexpected disruptions affecting these leading firms can trigger outsized volatility and losses across passive portfolios that mirror headline indices. While passive investing has gained popularity, the case for active management is stronger than ever.

In a fast-evolving technology sector where there are good reasons to hold certain dominant stocks, actively managed concentration offers significant advantages. Here’s an overview of those advantages and why the actively managed concentration approach of the Red Oak Technology Select Fund portfolio management team has proven especially effective.

Deep Fundamental Research and Enhanced Focus. Technology companies often have complex, rapidly changing business models. An active manager can perform deep, fundamental research to differentiate between companies with true, sustainable competitive advantages and those that are purely speculative. For the Red Oak Technology Select Fund, we rely on intense, specialized analysis to identify attractively valued, high-growth technology companies with business models featuring high barriers to entry that passive strategies might dilute.

“Concentrated portfolios allow active managers to focus on their best, high-conviction technology investment ideas, rather than diluting performance by holding lower-conviction stocks simply for diversification. In the Red Oak Technology Select Fund, we focus on industry leaders with a long-term outlook and an emphasis on those companies able to compound high returns on capital profit margins and cash flows .”

~ Robert Stimpson,

Chief Investment Officer and

Portfolio Manager of Oak Associates

Reducing Risk through Stock Selection. In the technology sector, returns are not evenly distributed, with sub-sectors often featuring “winner take all” dynamics. Further, technology stocks often trade at high valuations, making stock selection essential to identifying firms with genuine, long-term earnings potential. A concentrated portfolio allows active managers to avoid overexposure to hype-driven bubbles, overweight “winner” companies and exploit high performance dispersion. While holding fewer stocks might seem riskier, managed concentration mitigates overall portfolio volatility by selecting companies with strong fundamentals and low correlation to one another. The Red Oak Technology Select Fund employs a “financials-first” stock screening process, seeking valuation discipline, quality leadership, profitability, pricing power and stability.

“Red Oak Technology Select Fund is differentiated by its financials-first approach, employing a risk-averse strategy to tech investing by emphasizing valuation and fundamentals while avoiding hot trends, promises of next-generation or hyped disruptive innovation. This focus not only helps temper volatility but seeks to capitalize on the stock market’s version of compounded interest: highly profitable companies that reinvest their strong returns on equity. This approach tends to favor large-capitalization technology leaders with strong free cash flow and demonstrated respect for shareholder capital.”

~ Jeff Travis,

Portfolio Manager of Oak Associates Funds

Quality Over Quantity. Active managers can conduct deep research to find technology companies with sustainable competitive advantages and strong fundamentals, including healthy earnings, high free cash flow yield, high return on invested capital and low sales variability, in a sector prone to disruption. While concentration is often perceived as risky, active, disciplined management of a few high-quality companies can help reduce risk. When markets are heavily concentrated, passive strategies may inadvertently expose investors to unexpected risks should market leadership rotate or if those few dominant stocks underperform. The Red Oak Technology Select Fund normally holds 20-30 securities in 5-8 technology sub-sectors and employs a sell discipline as key to its performance as its selection criteria.

Real-Time, Tailored Adaptability and Agility. The technology sector is volatile, experiencing rapid shifts in innovation cycles, themes and company leadership. Active managers can identify turning points and quickly adapt to emerging trends, strategically allocating capital toward specific high potential “new economy” segments. Intentionally designing selective concentration exposure, the Red Oak Technology Select Fund’s representative themes include enterprise capital technology spending, digital media advertising, semiconductor proliferation, electronic finance and cybersecurity.

“There are valid reasons for ownership of certain Magnificent 7 securities in a technology portfolio. The Red Oak Technology Select Fund will typically hold positions in some, though not all, of them, and we actively adjust those positions opportunistically for advanced long-term trend positioning and without regard to benchmark weightings.”

~ Robert Stimpson,

Chief Investment Officer and

Portfolio Manager of Oak Associates

From an individual stock perspective, managed concentration enables mitigation of “winner’s curse,” managed risk during sector pullbacks and reduction in the crowding that has become typical, as reflected in the high top-end concentration of some major passive, market-weighted indices. Active managers can adjust weightings—add to positions as valuations and long-term prospects become attractive, take off gains, exploit market inefficiencies, reduce exposure to or completely exit overvalued or overweighted stocks and dynamically and purposefully re-balance positions without regard to raw market forces—providing a defensive advantage that index tracking funds cannot. While the Red Oak Technology Select Fund typically holds positions in some, but not all, of the Magnificent 7 stocks, our managed portfolio offers daily oversight and the ability to pivot rapidly at market inflection points in response to market pullbacks or shifting trends and allocate away from incumbent, disrupted firms to new leaders, particularly useful for navigating the fast-paced, high-beta technology sector.

Higher Potential Alpha Generation. At Oak Associates, we believe that a concentrated portfolio of financials-first technology sector “best ideas” leads to higher potential Alpha generation. For the latest holdings, attribution and performance of the Red Oak Technology Select Fund, please visit https://www.oakfunds.com/strategies/red-oak-technology-select/.

1 “U.S. Equities, December 2025,” S&P Dow Jones Indices Market Attributes.

2”Stock Market Concentration Has Surpassed Its 1930s Peak. Should Investors Worry?,” Morningstar, February 27,2026. As a % of S&P 500 Market Cap graph data source: Bloomberg as of 3/9/2026.

For more mutual fund information, call today: 1-888-462-5386 or visit our website at www.oakfunds.com

Past performance is no guarantee of future results. Oak Associates Funds are available to U.S. investors only. The thoughts and opinions expressed in the article are solely those of the author as of March 11, 2026. The referenced indices are for illustrative general market comparisons only and not meant to represent performance of any fund. Investors cannot invest directly in an index.

Alpha–the excess return of an investment relative a benchmark index, when adjusted for risk.

For a complete list of Red Oak Technology Select Fund holdings, please visit the Forms & Information page of our website: https://www.oakfunds.com/forms-information/

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Funds’ prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

Mutual fund investing involves risk, including the possible loss of principal. Oak Associates Funds are distributed by Ultimus Fund Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

20260311-5292906

More News & Insights