2025 Second Quarter Market Commentary

Commentary

Uncertainty 2.0: Resilience Amid Evolving Challenges

The US equity markets have shown remarkable resilience in 2025 despite the ongoing turbulence. After a first quarter decline of 4% in the S&P 500 Index, the second quarter delivered a robust 10.6% rebound, reaching a new all-time high. However, the journey was far from smooth: from mid-February peaks to early April lows, the market endured a nearly 19% drop, driven by concerns over initial tariff proposals and escalating trade tensions, as noted in our first quarter commentary ‘The Only Certainty is Uncertainty’.

Since April, the market has surged more than 24%, bolstered by progress in trade negotiations that eased fears of worst-case scenarios. Yet, new uncertainties loom, including a critical tariff deadline in July, the approval process for the proposed budget bill, and rising geopolitical tensions in the Middle East. Volatility has risen and is likely to persist as investors navigate these evolving challenges in the second half of 2025.

Despite these headwinds, both the economy and equity markets have demonstrated strength, with emerging tailwinds offering promise. The recent rally has been fueled by improved clarity stemming from easing trade tensions with China, a pause in reciprocal tariffs, and corporate earnings that have surpassed expectations. Although sector performance has remained uneven, investor sentiment has improved in response. Technology stocks staged a strong comeback in the second quarter after lagging in the first three months of the year, while traditionally defensive sectors—such as Healthcare and Consumer Staples—underperformed on a relative basis.

Recession concerns have eased as severe trade policy scenarios appear increasingly unlikely. However, economic data may remain volatile as the inventory build-up triggered by early-year tariff anticipation continues to cycle through the system. Housing affordability remains a headwind to growth, pressured by both elevated mortgage rates and home prices. A lesser-discussed potential catalyst, however, is the proposed budget bill’s provision for immediate expensing of capital investments, which could significantly boost corporate spending, driving economic growth, job creation, and consumer activity.

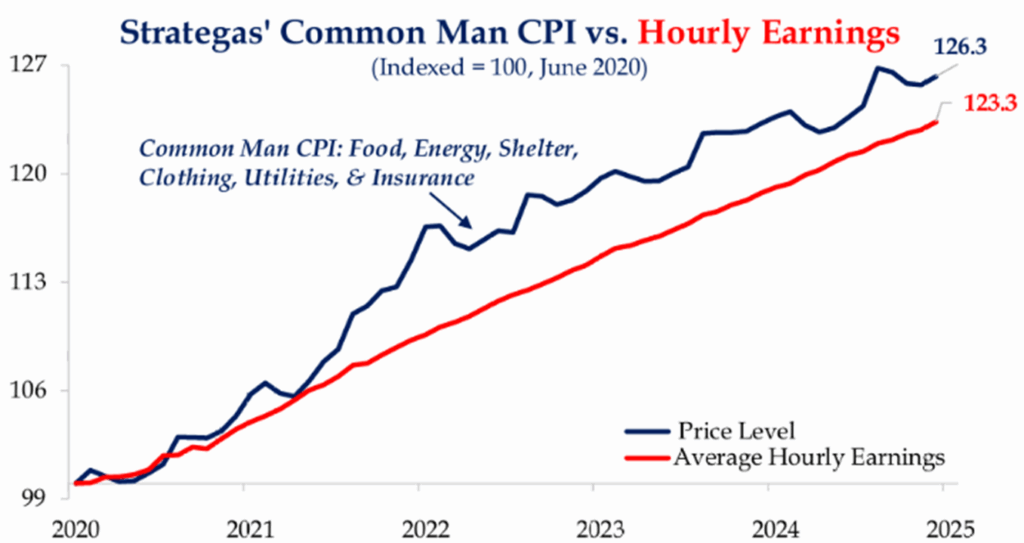

A robust labor market and steady wage growth have continued to underpin consumer spending and overall economic expansion. However, momentum has slowed as consumers have exercised greater caution amid ongoing tariff-related uncertainty. While tariffs typically represent a one-time price adjustment rather than persistent inflation, they come at a particularly challenging time—layered on top of several years of elevated price pressures that have already strained household budgets, especially for lower-income families. The chart below, which we have referenced previously, helps illustrate this dynamic.

Source: Strategas, BLS, HaverIn an effort to explain the disconnect between a healthy labor market and declining consumer confidence, the economic research firm Strategas developed the “Common Man CPI.” This alternative inflation measure breaks out spending on essentials—such as food and energy—from discretionary items like dining out and jewelry. As shown in the chart, while wages (red line) have indeed increased, they have not kept pace with the rising costs (blue line) of day-to-day necessities. This divergence may help explain why consumers remain uneasy, particularly with the potential implications of tariffs still on the horizon.

While the post-Covid surge in prices persists, annual inflation has remained modest, hovering just above the Federal Reserve’s 2% target level. The ‘rents’ component, a lagging indicator of housing costs, has taken longer to adjust but continues to exert downward pressure on overall inflation. Lower energy prices have also played a significant role in keeping inflation in check. After a brief spike following Israel’s initial strikes against Iran, the recent cease-fire has brought prices back down. In the near-term, geopolitical developments and the outcomes of tariff negotiations are likely to be the primary drivers of inflation trends.

Thus far, the economy and financial markets have adapted to evolving uncertainties with notable resilience. Although economic and earnings growth has moderated, both remain in positive territory. Tariff-related disruptions are expected to exert some influence but appear well-contained relative to early worst-case projections. Many of the prevailing uncertainties are now well understood, with increased clarity anticipated in the months to come.

Looking further out, structural tailwinds offer reasons for optimism. Business investment in artificial intelligence was already supporting capital expenditures, and the provision for immediate expensing of manufacturing structures, software, new equipment, and R&D investments—currently included in the proposed budget—would further incentivize corporate spending. Increased investment lays the groundwork for stronger GDP performance and productivity gains. A stronger economy supports employment and consumer spending, creating a favorable environment for earnings growth and equity markets.

Finally, please visit our new website at WWW.OAKFUNDS.COM. As always, thank you for reading and please do not hesitate to reach out to us if we can assist you with achieving your investment goals in any way.

Kind Regards,

Jeff Travis, CFA

Portfolio Manager

Oak Associates, ltd.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell. This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization-weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.