The Power of Profitability: What Differentiates Large-Cap Tech from the Rest of the Stock Market

Insights

More than almost any other financial analysis metric, high and sustainable profitability presents several distinct advantages when considering a company’s viability for long-term investment success. In our opinion, profitability, whether defined as return on assets (ROA), return on invested capital (ROIC) and return on equity (ROE), has been a distinguishing characteristic that underscores the large-cap technology sector returns over the past decade relative to the broader market and the rest of the technology universe. How efficiently a company generates profits has proven to be more determinant and consistent than valuation metrics or earnings growth rates for long-term outperformance. Stock markets can cycle between favoring value stocks or high-growth companies. Yet with a focus on profitability, the market’s style preference is less relevant.

The Power of Profitability creates a distinct advantage for companies and offers both strong offensive and defensive characteristics that investors should exploit for long-term outperformance.

The ability to redirect excess profits into incremental growth areas provides both powerful flexibility and opportunity. Large companies blessed with high profit-margins businesses are able to reinvest those returns in new areas and growth initiatives with a long-term perspective. This creates an offensive advantage that smaller companies or less profitable competitors lack. Expanding product lines, entering new markets, investing in research and development and/or making acquisitions are possible if there are funds available for reinvestment. For more than a decade now, a handful of mega-cap technology companies in the S&P 500 Index have dominated the contribution to returns of the benchmark index, due to the combination of their performance and weight in the broad market index. Yet, the Magnificent Seven as they are known, also boast enviable high margins and high return-on-equity businesses, enabling their reinvestment of capital into artificial intelligence (“AI”), semiconductor chips, cloud computing, storage and other growth areas at a pace and depth that put them into a position of dominance.

The ability to reinvest excess profits empowers corporate transformation. Once a company becomes a well-established market leader, it must adapt to remain dominant despite maturing business models. Historically, investing in the largest 10 stocks in the S&P 500 was a recipe for underperformance. Yet, for more than a decade now, the “largest-of-the large” have been able to thwart the size curse by exploiting their extreme profitability to empower change. Microsoft leveraged its near operating system monopoly and its Office productivity suit, into gaming, cloud applications and web services. Apple pivoted from computers into iPhones, tablets, accessories and platforming mobile applications. Facebook parleyed free social networking into targeted advertising, Instagram and Reels. Google migrated from search and keyword advertising to Youtube, online services, software and cloud computing. Superior financial efficiently enables companies to defend, adapt, and retain their leadership positions.

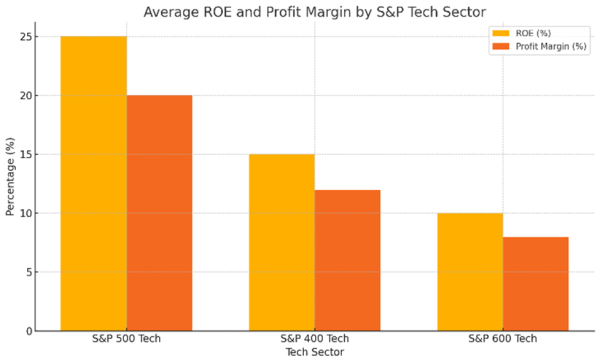

High margins produce strong, steady cash flow allowing for superior return of capital to shareholders. Whether through stock buybacks or increased dividends, high cash flow provides companies with opportunities to reward their shareholders, who often favor the tax benefits, predictability and distributions of returns of capital. Notably, large-cap technology companies have generated free cash flow margins superior to the rest of the U.S. stock market. * Returning capital to shareholders demonstrates a similar financial stewardship desired by dividend investors. Companies can also act as incremental buyers of their own shares when markets fall. Given the use of stock-based compensation practices at technology companies, offsetting the growth in share count through repurchasing is also important, as it preserves and enhances earnings-per-share growth.

Albert Einstein said, “The most powerful force in the Universe is compound interest.” In the equity market, high-profit margins and efficency are the fuel that feed the stock market’s version of compounded interest. Put simply, companies that earn high returns-on-capital, redeploy these proceeds back into their high-return-on capital business model. And unlike fixed-income compounding investments with moderate yields, high-margin technology companies can reinvest at significantly higher internal rates of return.

High levels of profitability provide a defensive advantage amid uncertain market conditions. High profit margins can provide a level of security and reliability not often seen in the U.S. equity market. Why? Because, by definition, high profit margins enable a company to retain a larger portion of its revenue as earnings. This can enhance financial stability, improving their potential to weather economic downturns, withstand upward pressure on expenses and manage unexpected costs. It provides a cushion that can support ongoing operations and strategic investments even during challenging times. While large-cap technology companies are not immune to broad market corrections, the ability to tolerate earnings volatility is beneficial. Indeed, the sector’s resilience owes much to the fact that mega-cap technology companies tend to have high quality balance sheets and low leverage. In periods of economic distress, excessive debt, high-interest costs and negative earnings are a common formula for insolvency and collapse.

Profitability provides large-cap technology companies with both offensive and defensive advantages.

High-profit margin businesses enable companies to operate independently of the capital markets. The era of easy, inexpensive money experienced during much of the 2000s—until the last year and a half or so—is over, and even as the U.S. Federal Reserve begins to cut borrowing cost, interest rates and the cost of private credit are likely to stay elevated for some time. Highly profitable companies that can avoid reliance on the capital markets are in an advantaged position, especially compared to smaller-cap companies more dependent on external financing. Today, the technology sector has largely been able to self-sufficiently fund growth. This is in stark contrast to conditions seen in the late 1990s when the adoption of the Internet saw capital flow freely, especially to start-up companies that had no track record of success. Yet when the dot.com bubble burst, capital dried up and unprofitable companies, and those reliant on external funding, led the collapse. For over two decades now, the Federal Reserve has suppressed the cost of capital inadvertently through its quantitative easing actions. With the arrival of high inflation following the Covid pandemic, a return to easy money policies is not viable.

High profitability is the stock market’s best example of compounded interest.

Profitability, the flexibility it creates, and the economic ammunition it produces is a serious competitive advantage. We often say the biggest competitive threat companies face is not a rival’s innovation or even a new entrant across the street. Rather, the biggest competitive threat to any business is time and money. In technology, that threat is outsized. Those companies that have deep pockets, via high profitability, and long-term horizons have the resources and strategic tools that others do not. Within the various technology sectors, smaller-cap software, AI, security and search companies will struggle to compete with their larger-cap counterparts over the long run given the investment required to dominate in these areas, as the cost of entry is immense. A software company may have a newer, slicker, faster interface or feature set, but rest assured, Microsoft, Google, Amazon, or Apple, etc., will be updating their products. It may take several iterations for the tech giants to outdo smaller more nimble competitors, but eventually, with time and money, they succeed. Just ask Netscape (browser), Yahoo (search), Blackberry (phones), Napster (music), AOL (ISP), and more and more. Over time, larger-cap technology companies with demonstrated profitability have both the balance sheet and efficient, effective business models to sustain their leadership position.

Success breeds competition. But for mega-cap tech, high profitability and reinvestment into their own growth helps sustain that success.

Interested in More Info?

For questions or to speak with the Oak Associates Funds’ Relationship Manager, contact Sarah Hill at 330-819-3308 or shill@oakassociates.com.

Check out our News & Commentary at oakfunds.com for updates on the Oak Associates Funds.

For mutual fund information, call today: 1-888-462-5386 or visit our website at www.oakfunds.com.

Past performance is no guarantee of future results. Oak Associates Funds are available to U.S. investors only. The thoughts and opinions expressed in the article are solely those of the author as of September 1, 2024. To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Funds’ prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money. Mutual fund investing involves risk, including the possible loss of principal. Funds that emphasize investments in technology generally will experience greater price volatility. There are additional risks associated with investing in a single-sector fund, including greater sensitivity to economic, political, or regulatory developments impacting the sector. Information technology companies face competition and potentially rapid product obsolescence.

Return on Equity (ROE) – A measure of a company’s return on net assets.

Return on Invested Capital (ROIC) – A measure of a company’s efficiency in allocating capital to generate profits.

Portfolio holdings are subject to change and should not be considered investment advice. The portfolio holding information is as of 6/30/2024. Red Oak Technology Select Fund Top 10 holdings as a percent of assets were: Alphabet 10.23%, Amazon 7.48%, KLA Corp 7.35%, Microsoft 6.54%, Synopsys 5.77%, Oracle 5.45%, NVIDIA 5.45%, Meta 5.43%, NXP Semiconductors 4.49% and Qualcomm 4.49%.

Oak Associates Funds are distributed by Ultimus Fund Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

Related Information – Download File Here

More News & Insights