Shifting Your Clients’ Perspective Amid Volatile Markets

Advisor Resources

As uncertainty has heightened, driven by macroeconomics, monetary policy, pandemic overhangs, geopolitics and more, investors have grown increasingly wary. Exacerbating your clients’ concerns is the oft-dramatic coverage the media presents on the drivers of market volatility. While concerns are valid, there are positives as well, and now is an exceptionally opportune time for advisors to strengthen client relationships by providing fact-based perspective.

To help you engage in conversations that reinforce your value as an advisor—ones that help clients put risks in context, reinforce long-term goals and reveal biases that may make them vulnerable to poor investment decisions, we explore here the current “hot topics” and provide some specific actions your clients might want to consider.

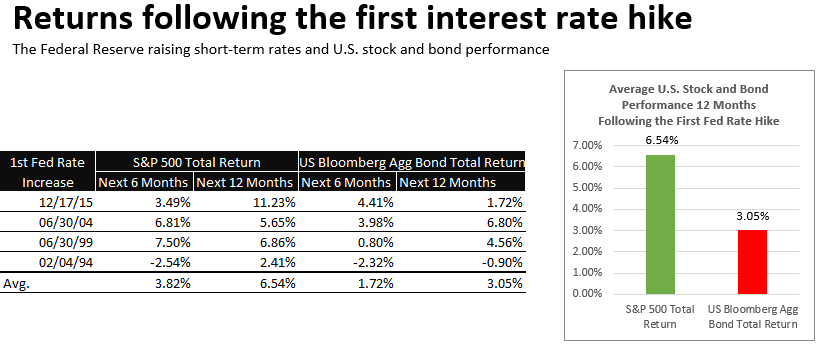

Rising Interest Rates After an extended span of near-zero interest rates, the U.S. Federal Reserve (Fed) raised the targeted federal funds rate five times in the first nine months of 2022 to a range of 3.00% to 3.25% as inflation persisted at multi-decade highs.

- Shifting Perspective: While the media focuses on how higher interest rates affect mortgages, credit cards, car loans, etc., what rarely gets mentioned is that higher interest rates mean better savings rates. For those investors who already hold a portion of assets in cash and rely to some degree on interest from savings accounts, certificates of deposit (CDs) and other interest-bearing instruments for supplemental income, higher interest rates are a plus! Further, looking at the past 50 years or so, it’s actually zero interest rates, not higher interest rates, that have been the true aberration to history.

- Interesting Fact to Share: Rising interest rates do not have a direct correlation to stock prices. However, when interest rates move higher, stocks can sometimes fall out of favor or become increasingly volatile because higher rates affect companies’ ability to borrow and pay off debt. Also, when interest rates rise, consumers and companies alike typically curb their spending, which can result in lower stock prices. Notably, however, stocks have historically performed better during periods when interest rates are rising—when looked at 12 months following the first rate hike by the Fed.1 After all, interest rates are being hiked by the Fed to slow—not stop—the rate of economic growth, and a strong economy can be good for companies.

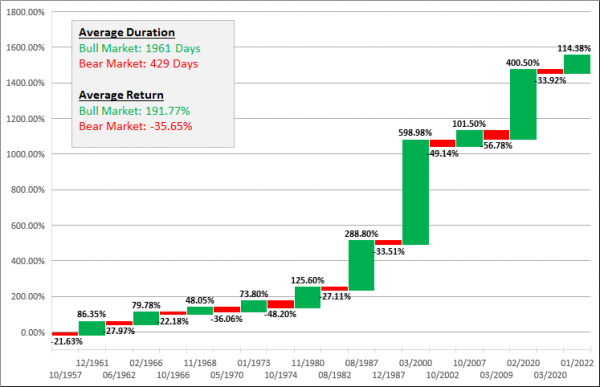

Bear Market Returns: The U.S. equity market had its worst first half of a year in 2022 since 1970, erasing nearly all the gains of 2021, with the S&P 500® Index officially entering a bear market on June 13, 2022. The third quarter of 2022 extended the losses, with the S&P 500® Index posting its worst first nine-month start to a calendar year since 2002.

- Shifting Perspective: While bear markets can impose challenges to your clients’ financial goals, we need to remember that bear markets are a normal and inevitable part of stock investing. And just as bull markets are followed by bear markets, bear markets are followed by bull markets. Only time will tell if the 2022 downturn in the S&P 500® Index was a bear market within the long-running secular bull market that began in March 2009 or not. A variety of factors will affect market direction—for example, policymakers’ effectiveness in managing inflation; geopolitical events, such as the Russia/Ukraine war; and investors’ expectations around those factors. Either way, a bear market is neither the time to disrupt long-range plans by going to the sidelines nor a reason to stop investing.

- Interesting Facts to Share: Historically, bear markets have appeared every six years on average, with the S&P 500® Index experiencing 17 bear markets since 1926, most recently in March 2020.2 Further, half of the S&P 500® Index’s strongest days in the 20 years between December 2001 and December 2021 occurred during a bear market. Another 34% of the S&P 500® Index’s best days took place in the first two months of a bull market—before it was clear a bull market had begun.3 Bear markets have historically varied in length but the average bear market lasted approximately 15 months.4 Importantly, stock markets have always recovered—every time.

Inflation After years of Consumer Price Index (CPI) readings below 2%, financial markets have been operating against a backdrop of inflation that rose to a high of 9.1% year over year in June 2022, the largest 12-month increase since the period ending November 1981. While CPI readings have since fallen to 8.2% for September 2022 (latest data available), they remain high.

- Shifting Perspective: When thinking about where to invest during periods of high inflation, most of your clients likely think about Treasury inflation-protected securities (TIPS) and commodities, especially gold. But you might suggest your clients consider increasing their allocations to equities as a way to tilt their investment portfolios to position for high inflation. Inflation may cause short-term market volatility. But many companies, despite rising input costs, have an ability to increase prices on consumers to maintain profit margins, enabling earnings expectations to remain strong. This is especially true for basic items of necessity—consumer staples, utilities, health care. Further, bonds do not historically perform well during an inflationary period, leaving equities or the sidelines among the few viable choices. While overall annual U.S. equity returns are forecast to be lower over the next decade, they are still widely expected to exceed those of other key asset classes.

- Interesting Fact to Share: The average annual return of the S&P 500 Index was 11.70% over the 10-year period ended September 30, 2022 and was 10.51% since the inception of the S&P 500 Index in 1926. These returns exceed the high U.S. inflation rates seen in 2022.

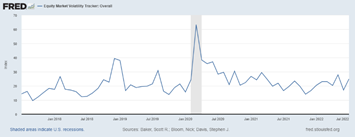

Equity Market Volatility: U.S. equity market volatility, as measured by the S&P 500 Index, for 2022 year-to-date through September was 1.85% as compared to 0.97% in 2021, 1.73% in 2020, 0.85% in 2019, 1.21% in 2018 and 0.51% in 2017, which was the low since 1962.5.

- Shifting Perspective: While equity market volatility so far this year has been somewhat higher than it was in 2021, the data shows it’s not as dramatic as it might feel. Further, volatility can be healthy, helping to remove the froth from a market that may be running too far ahead of itself and bringing asset prices back in line with underlying fundamentals. To prepare clients for volatile markets, perhaps keeping in mind that while equity market volatility can not be controlled, certain other factors such as portfolio diversification, rebalancing and investment time horizons can be controlled. And emotionally-driven behavior can be more devastating to a portfolio than virtually any market volatility. So, a focus on what can be controlled can effectively minimize the impact of volatility. Finally, it’s well worth reminding your clients that to time the market, they would need to be right not once, but twice—when to get out of the market and when to get back in. To do this consistently is simply improbable for any investor, any portfolio manager, any advisor.

- Interesting Fact to Share: Despite an average intra-year drop of 14.6%, annual returns of the S&P 500 Index were positive in 24 of the past 31 years through 2021.6

Some Actions You Might Suggest Your Clients Take

In times like these, providing advice goes beyond asset allocation and retirement projections to include managing client behavior. Amid volatility, your clients need to trust you more than ever, and they need to see you as a person of action. So, whether you sit with or call your clients during these times of market uncertainty, remember that you are not paid to be right all the time, but you are paid to reach out to them with an educated opinion based on experience. Managing client expectations is key. Here are some actions you might suggest they consider in volatile markets to be able to knowledgeably and comfortably stay invested.

Use dollar-cost averaging. As you well know, with this approach, your clients will be buying more shares when prices are low and fewer shares when prices are higher—regardless of how the market is performing. If you shift your clients’ perspective from one of “throwing good money after bad” during a downturn toward focusing on potential gains by buying more shares of funds with the same dollars they’ve always invested, bear markets can be good opportunities.

Avoid acting on emotions. Fear and greed are probably the emotions that most get in the way of prudent investment decisions, causing many people to lose money in the stock market. While such emotions are normal, controlling them is the key. A good rule to remind new investors, those nearing retirement, and retirees alike is that if their decision to buy or sell cannot wait for a few days, they are likely making an emotional or reactive decision. They should sleep on it. Digest. Find out more. Consult with you, their advisor. Then make a grounded decision.

Focus on diversification. A balanced, diversified portfolio, both by asset class and within the equity market itself, can’t guarantee your clients will never have losses, as was the case during the first nine months of 2022 when both equity and fixed-income markets declined. But the fundamental logic underlying diversification is still sound, potentially providing portfolios a downside cushion. It’s a time-tested, valuable strategy, bear market, volatile market or not.

Get out of the habit of checking your balances frequently. Going through a stretch of disappointing equity market returns can be stressful. While it is important to stay informed, watching the daily, weekly or even monthly moves of the market can be detrimental to the long-term investment mindset. And remember, no one actually loses money unless or until they sell.

Revisit risk tolerance. If the bear market of 2022 is causing your clients extreme anxiety, then maybe their risk appetite is smaller than previously thought. Speaking with you as their financial adviser, who hopefully understands their situation and also brings an objective view to decision-making, can be helpful.

Keep doing what you’re doing—with a long-term perspective. For many investors, seeing negative signs in their shareholder reports can be alarming and prompt an emotional urge to pull their money out to avoid further losses. But this is not an effective strategy. Even clients who have been through multiple market downturns and know the facts intellectually will have that instinct to make what would be counter-productive decisions. The best advice you can give your clients is 1) their long-term plan was designed to withstand inevitable market slumps and 2) it’s old but true—time in the market is better than timing the market. It’s been proven study after study after study. The lessons from each are to stay invested and remember the benefits of long-term investing.

The Opportunity Cost of Market Timing Rather Than Time in the Market is Dramatic

| $10,000 invested in the S&P 500 | (value at end of period 12/31/06 – 12/31/21; annualized returns) |

|---|---|

| Staying Fully Invested | $45,682 | 10.66% |

| Missed 10 Best Days | $20,929 | 5.05% |

| Missed 20 Best Days | $12,671 | 1.59% |

| Missed 30 Best Days | $ 9,033 | -0.68% |

| Missed 40 Best Days | $ 5,786 | -3.58% |

Source: Bloomberg.

* * *

In short, keeping volatile markets in perspective is critical for both you and your clients. While telling your clients to do nothing may be difficult, taking the time to remind them that if they already have a well-diversified portfolio consistent with their investment timeline, personal circumstances, and risk tolerance, there is little incentive to deviate from their financial plan. Staying the course and staying calm with a goals-based approach may be the best strategy of all, regardless of market conditions.

FOR FINANCIAL PROFESSIONAL USE ONLY

Sources

1 Bloomberg Finance L.P. Total Return for S&P 500 Index and U.S. Bloomberg Aggregate Bond Total Return Index, 02/04/94 to 12/17/15. Retrieved from Bloomberg database.

2 Fidelity, “Bear market basics,” June 28, 2022.

3 Ned Davis Research, 12/21. Time period referenced is 12/16/01–12/15/21.

4 Schwab Center for Financial Research, “Bear Market: Now What?,” July 13, 2022.

5 S&P Dow Jones Indices, “Market Attributes: U.S. Equities,” September 2022.

6 Bloomberg Finance L.P. S&P 500 Total Return 12/31/06 to 12/31/21. Retrieved from Bloomberg database.

Interested in More Info?

For questions or to speak with the Oak Associates Funds’ Relationship Manager, contact Sarah Hill at 330-819-3308 or shill@oakassociates.com.

Oak Associates Funds Family

White Oak Select Growth Fund (WOGSX)

Pin Oak Equity Fund (POGSX)

Rock Oak Core Growth Fund (RCKSX)

River Oak Discovery Fund (RIVSX)

Red Oak Technology Select Fund (ROGSX)

Black Oak Emerging Technology Fund (BOGSX)

Live Oak Health Sciences Fund (LOGSX)

About the Oak Associates Funds

Oak Associates Funds is a family of seven no-load equity mutual funds. All Oak Associates Funds are domestic U.S. equity portfolios and follow the firm’s tradition of concentrated, low-turnover, long-term oriented investing. The fund strategies are distinguished from each other by their sector concentrations and the market capitalization of the stocks in which they invest.

Check out our News & Commentary at oakfunds.com for updates on the Oak Associates Funds.

For more mutual fund information, call today: 1.888-462-5386 or visit our website at www.oakfunds.com

Past performance is no guarantee of future results. Oak Associates Funds are available to U.S. investors only. The thoughts and opinions expressed in the article are solely those of the author as of September 1, 2024. To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Funds’ prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money. Mutual fund investing involves risk, including the possible loss of principal. Funds that emphasize investments in technology generally will experience greater price volatility. There are additional risks associated with investing in a single-sector fund, including greater sensitivity to economic, political, or regulatory developments impacting the sector. Information technology companies face competition and potentially rapid product obsolescence.

Return on Equity (ROE) – A measure of a company’s return on net assets.

Return on Invested Capital (ROIC) – A measure of a company’s efficiency in allocating capital to generate profits.

Portfolio holdings are subject to change and should not be considered investment advice. The portfolio holding information is as of 6/30/2024. Red Oak Technology Select Fund Top 10 holdings as a percent of assets were: Alphabet 10.23%, Amazon 7.48%, KLA Corp 7.35%, Microsoft 6.54%, Synopsys 5.77%, Oracle 5.45%, NVIDIA 5.45%, Meta 5.43%, NXP Semiconductors 4.49% and Qualcomm 4.49%.

Oak Associates Funds are distributed by Ultimus Fund Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

Related Information – Download File Here