2026 Second Quarter Market Commentary

Commentary

Economic Resilience Wins the First Half

As the World Cup kicks off and nations vie for glory on the pitch, a different kind of competition has been playing out within financial markets all year. Throughout the first half of 2026, the match between geopolitical disruption and economic resilience has been a back-and-forth affair. Equity markets scored the first quarter negatively as the outbreak of the conflict with Iran drove oil prices and inflation fears higher which sent the S&P 500 lower. Despite this setback, the second quarter countered strongly, driven by resilient economic fundamentals, better than expected corporate earnings and hopes for de-escalation of events in the Middle East. At the half, market performance suggests investors have chosen to look beyond unfavorable geopolitics for now with the S&P 500 rising 15% during the period and nearly 10% for the year.

The story of the first half was how well corporations were able to absorb economic challenges. Years of adapting to pandemic disruptions, supply chain bottlenecks, labor shortages, and inflationary spikes have left many companies with stronger balance sheets, healthier margins, and a greater ability to adjust quickly. Those experiences have made businesses better prepared to navigate uncertainty and resilience that have shown up in recent earnings.

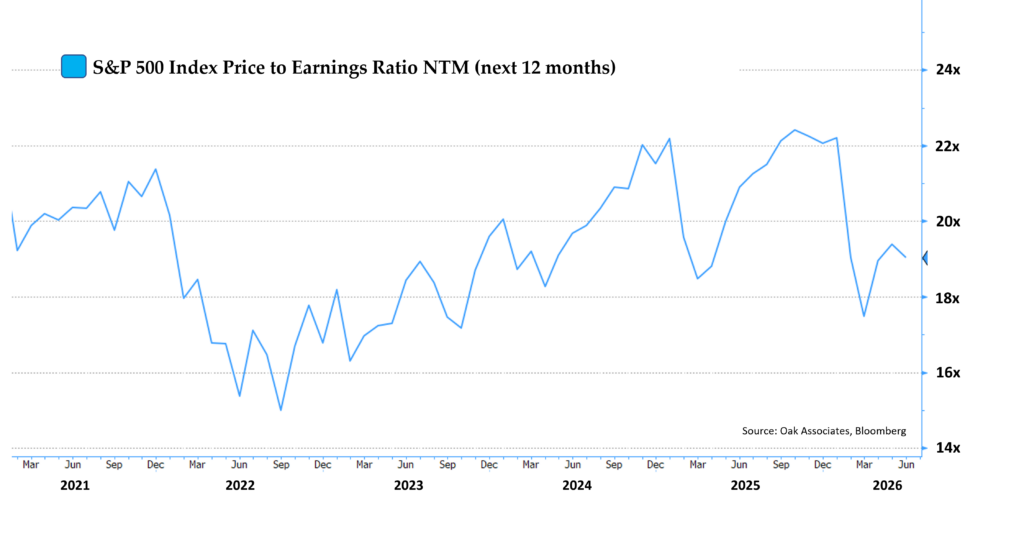

Throughout the second quarter, companies reported first-quarter earnings that came in better than predicted. S&P 500 earnings grew by more than 25% year-over-year, and revenues also contributed strongly, rising more than 10%. These strong fundamentals pushed profit margins to record highs of nearly 15% and were the driving force behind the equity market’s advance. This is an important characteristic as it means equity returns have been driven by earnings growth rather than expanding valuations. The S&P 500’s forward price-to-earnings multiple has actually compressed (as seen in the chart on the following page), falling from roughly 22x at the start of the year to below 20x — even as stock prices moved higher. Companies essentially “grew into” their valuations.

The labor market has provided an important source of stability due to those favorable corporate fundamentals. While hiring has cooled from the rapid pace of prior years, widespread job losses have not materialized. The environment has evolved into one of low hiring and low firing. This is supported by structural labor supply constraints and continued strong participation rates that suggest a dramatic change is unlikely. Historically, significant economic slowdowns have often been accompanied by broad deterioration in employment conditions.

Artificial intelligence (AI) related spending also remains a core support for both earnings and economic activity. Lately, investors have questioned whether AI-related investments have become excessive. Instead, the capital spending cycle associated with AI accelerated further with hyperscale technology companies continuing to invest aggressively in data centers, cloud infrastructure, semiconductors, and software capabilities. Leadership has also widened somewhat beyond the largest growth stocks as industrial companies connected to power generation, infrastructure expansion, electrical equipment, and manufacturing have also benefited from the AI‑driven buildout.

Inflation, however, continues to be the most visible macroeconomic risk. The conflict involving Iran created a shock in the quarter by threatening the flow of oil and other critical commodities through the Strait of Hormuz. Rising energy prices quickly revived memories of the inflation surge experienced earlier this decade and raised concerns that a second inflation wave could emerge. Higher energy costs worked like a tax on consumers, lifting transportation costs and diluting the tailwinds associated with the “One Big Beautiful Bill” fiscal package. Even so, underlying inflation outside energy proved more constructive: wage pressures moderated, and shelter inflation showed improvement. While oil and gasoline prices are higher, the market is concluding that the cessation of hostilities in Iran will lead to lower energy costs six to nine months from now. This would allow the Fed to stay data‑dependent and on hold rather than tightening.

The consensus entering 2026 leaned toward a “Goldilocks” outcome of solid growth, easing inflation, and support from positive changes to both monetary and fiscal policies. Midway through the year, the backdrop is more complicated but still fundamentally resilient. The economy has absorbed a series of shocks driven by the Middle East conflict and its impact on the energy complex. As we look toward the second half of 2026, both opportunities and risks remain.

Going forward, we expect the current environment to continue along a slower, uneven expansionary path in which earnings and investment keep the economy growing while inflation and geopolitics put a cap on valuation upside. If oil prices continue to retreat, inflation expectations stay anchored and labor-market data remains stable, the market has a credible path to a better second half driven by earnings, broader market participation, and improving investor confidence. Conversely, a re-escalation of tensions in the Middle East and renewed pressure on energy markets could challenge the resilience of the first half, giving way to a more difficult environment for both the economy and equities.

As always, thank you for reading and please do not hesitate to reach out to us if we can assist you with achieving your investment goals in any way.

Kindest Regards,

Jeff Travis, CFA

Portfolio Manager

Oak Associates, ltd.

Grow stronger together.

The investments referenced in this article may or may not align with those currently recommended or held by Oak Associates for itself, its associated persons, or on behalf of clients within the firm’s strategies as of the date indicated. These investments are subject to change. The mentioned investments do not necessarily represent all those bought, sold, or recommended to advisory clients over the past twelve months. Portfolios in other Oak Associates strategies may contain the same or different investments, due to factors such as varying investment strategies, client-specific restrictions, mandates, substitutions, liquidity requirements, or legacy holdings, among others. The investments highlighted were not selected based on their past performance. Readers should not assume these investments have been or will be profitable in the future.

Past performance is not a reliable indicator of future results. Investments can lose value, and there is no guarantee that any strategy or product will achieve its objectives or perform as anticipated. All investments involve risk, including the potential loss of principal. Before making any investment decisions, individuals should assess their risk tolerance and seek advice from a financial advisor. Information that is sourced from a third-party is assumed to be accurate but is not guarantee. This commentary does not constitute an offer or solicitation to buy or sell any financial products.

The S&P 500 Index is a well-known, market-capitalization-weighted index of 500 widely held U.S. equities, designed to reflect broad U.S. stock market performance.

CFA is a registered trademark of the CFA Institute.