Insights

2026 First Quarter Market Commentary

Commentary

April 2, 2026

Prior to the U.S.–Israeli attack on Iran, we expected U.S. equities to profit from a steady stream of economic stimulus and greater clarity around tariff policy. Consumers were likely to benefit from above-average tax refunds this season, while businesses stood to take advantage of accelerated depreciation rules and incentives to expand U.S.-based manufacturing. The pending change in leadership at the Federal Reserve could also have resulted in more administration-aligned, less restrictive interest rate policies.

This backdrop, combined with improved clarity regarding which countries and industries would face tariffs, and at what rates, should have provided a meaningful tailwind for U.S. equities. The stock market dislikes uncertainty and has consistently rallied on news that tariffs were lower than anticipated, delayed, or ruled unlawful. Settling the tariff question may have been welcomed by investors and businesses alike, as long-term strategic planning is difficult when import prices and cost structures change through executive action.

With the U.S. and Israel now engaged in a new geopolitical conflict in the Middle East, many of these tailwinds are being eroded by higher fuel prices, weakening sentiment, and rising inflationary pressures.

Revised 2026 Outlook

Historically, sharp spikes in energy prices have been a catalyst that pushed the U.S. economy into recession. While the U.S. economic base is resilient and diversified, energy prices have a uniquely broad influence, driving up input costs and squeezing consumers. A sustained surge in oil prices is therefore a very concerning development.

A short-term spike can be absorbed, but if energy prices remain elevated for a prolonged period, recession risk rises substantially. Consumers, who are highly sensitive to gasoline prices, will retrench, further slowing the economy. The duration of this conflict and the persistence of higher energy prices will be critical, even if the conflict ends quickly.

Oil Is Not the Only Problem

U.S. equities had been anticipating further easing of the tight monetary conditions imposed by the Fed to combat inflation following the COVID-19 pandemic in 2022. The Fed began an interest rate reduction cycle in September 2024 but has occasionally delayed additional cuts in order to assess the impact tariffs had on price levels. The Fed’s focus may now shift from a slowing job market and tariff-related inflation to energy-driven inflation. Instead of anticipating rate cuts, the market is now facing the possibility that the Fed may need an extended pause, or even raise rates, rather than continue lowering them.

This shift from potentially lower rates to rate increases is important because it affects company valuations, as future earnings are discounted using prevailing interest rate expectations. Rising rates can also alter investor risk appetite, making high valuations less attractive. This relationship underscores the 7% correction in the S&P 500 since the Iranian conflict began.

The Bond Market May Be the Ultimate Arbiter of Fiscal and Monetary Policy

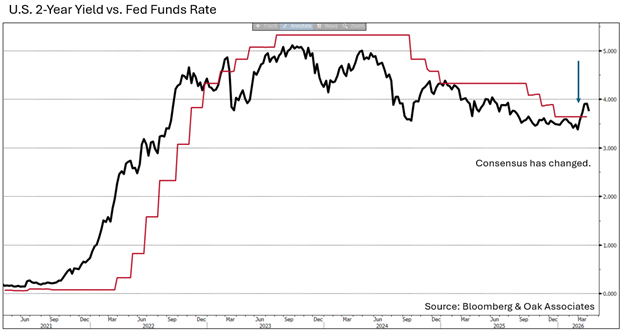

The yield on the 2-year Treasury is often a good representation of where market participants believe the Fed should set short-term interest rates. Historically, the 2-year yield has tended to anticipate the direction of future Fed policy.

Following the COVID pandemic, the 2-year yield indicated that the Fed was behind the curve and needed to raise rates to fight inflation. Conversely, over the past two years, the yield suggested the Fed could lower rates. Following the attack on Iran however, the market’s consensus appears to have shifted again. The 2-year yield now exceeds the Fed Funds rate, implying the market anticipates the Fed may tighten policy to confront renewed inflation.

Higher Interest Expense Is Restrictive

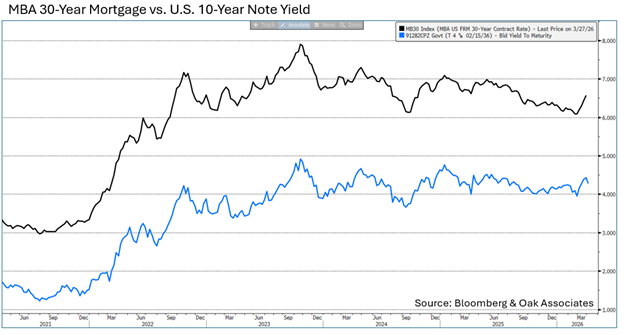

As equity investors, we naturally prefer stocks to fixed income securities, especially when inflationary pressures are elevated. However, the bond market is showing signs of stress that are likely to affect both the housing market and the broader economy. The yield on 10-year Treasuries, which strongly influences mortgage rates, has risen sharply in March. Mortgage rates have increased 50 basis points since the Iran conflict began, adding further stress to the housing market and reducing the economic stimulus typically provided by a strong real estate sector.

Overall demand for U.S. Treasuries has remained solid, but the mix of buyers suggests growing international concern about the U.S. fiscal situation. While both political parties spend heavily, they have very different approaches to increasing government revenue. Congress was determined to extend tax cuts, but receipts from tariffs anticipated to replace lost revenue are unlikely to be sufficient to offset the cost that the tax cuts may add to the deficit. Supply chains are already shifting to avoid import duties, and the legality of some tariffs (or refunds) remains unclear.

Questions about how the government will now pay for the tax breaks, while also spending a media-reported $1 billion per day on the Iran war, are certainly a concern for fiscal hawks. U.S. interest expense is already at record levels, with approximately 19% of tax receipts now going toward servicing outstanding debt, nearly double the level of five years ago. This situation puts upward pressure on bond yields and downward pressure on the U.S. dollar.

What We Are Doing to Manage Market Uncertainty

To navigate the change in the investment environment, particularly if energy prices remain elevated, we have been broadening sector exposure and trimming long-term winners with extended valuations. During periods of uncertainty, we tend to tilt further toward quality metrics and companies with durable earnings.

It is extremely difficult to predict whether this conflict will escalate or de-escalate quickly. Therefore, we believe it is prudent to remain invested in high-quality businesses with attractive long-term opportunities, while recognizing that initial oil and commodity supply disruptions may have lingering effects on the global economy. Stock prices have already recovered, somewhat reflecting the change in the economic risk profile. Given that the United States is fairly energy independent, the supply turmoil caused by a closure in the Straits of Hormuz would be more detrimental to Asian and European economies.

Stocks and Wars

Historically, U.S. equities have tended to tolerate military conflicts relatively well. For example, during the buildup to and initial invasion of Ukraine in 2022, the S&P 500 fell approximately 15% in the first half of 2022 but recovered quickly. It then went on to rise more than 90% over the following 3.5 years.

The Second Gulf War following the 9/11 attacks is more difficult to evaluate because it occurred amidst the dot-com bubble collapse and deep bear market. In this case, the market’s performance was influenced more by the economic cycle than by the conflict itself, which then persisted for more than 20 years in varying intensity.

During the First Gulf War in 1990, the S&P 500 fell roughly 16% in the first month of the war but recovered most losses by year-end and rose approximately 30% in 1991. Notably, that conflict was relatively short, something we hope proves true in this instance as well.

Conclusions

The outlook for 2026 has changed due to rising energy prices and the shift in investor expectations regarding Federal Reserve policy. The S&P 500 correction in March reflects this change in outlook and is consistent with declines seen at the onset of previous military conflicts. Many positives remain for U.S. stocks; specifically, the AI buildout continues, innovation and productivity remain strong, and stimulus from depreciation incentives and tax rebates is supportive. Historically, markets tend to look beyond military conflicts, and secular economic trends ultimately prevail.

While geopolitical conflicts create uncertainty and short-term volatility, history suggests markets ultimately follow earnings, interest rates, and economic growth. The key variable today is global energy prices. If oil prices retreat, this may prove to be a temporary correction. If energy prices remain elevated for an extended period, recession risks rise. Until that becomes clearer, we believe a higher-quality, more defensive posture is warranted while remaining fully invested for long-term growth. Our base case remains that the conflict is brief and supply disruptions are moderate. We acknowledge that risk aversion is rising, and we believe it is prudent to protect profits and emphasize more defensive portfolio characteristics. We believe stocks remain preferable to bonds, and the U.S. economy is less exposed to energy risks than other international markets.

As always, we are available to answer client questions and look forward to speaking with clients, advisors, and consultants. Please feel free to reach out at any time.

Kind Regards,

Robert Stimpson, CFA

Chief Investment Officer

Oak Associates, ltd.

Grow stronger together.

The investments referenced in this article may or may not align with those currently recommended or held by Oak Associates for itself, its associated persons, or on behalf of clients within the firm’s strategies as of the date indicated. These investments are subject to change. The mentioned investments do not necessarily represent all those bought, sold, or recommended to advisory clients over the past twelve months. Portfolios in other Oak Associates strategies may contain the same or different investments, due to factors such as varying investment strategies, client-specific restrictions, mandates, substitutions, liquidity requirements, or legacy holdings, among others. The investments highlighted were not selected based on their past performance. Readers should not assume these investments have been or will be profitable in the future.

Past performance is not a reliable indicator of future results. Investments can lose value, and there is no guarantee that any strategy or product will achieve its objectives or perform as anticipated. All investments involve risk, including the potential loss of principal. Before making any investment decisions, individuals should assess their risk tolerance and seek advice from a financial advisor. Information that is sourced from a third-party is assumed to be accurate but is not guarantee. This commentary does not constitute an offer or solicitation to buy or sell any financial products.

The S&P 500 Index is a well-known, market-capitalization-weighted index of 500 widely held U.S. equities, designed to reflect broad U.S. stock market performance.

CFA is a registered trademark of the CFA Institute.