2025 Third Quarter Market Commentary

Commentary

Beyond the Sand

The stock market is not the underlying economy. While they are connected, their relative performance often diverges for a variety of reasons. As it relates to the current quarter, US equities continue to look beyond the risk of tariffs, weakening unemployment data and the threat of inflation, in favor of the benefits that a Federal Reserve interest-rates-easing cycle could produce. This does not suggest the market is ignoring the near-term risks, simply that it is more focused on the economic benefits which AI innovation might create, the capital spending surge it is fueling, and the stimulative lifeline a more accommodative Federal Reserve may enable.

Year-to-date, the S&P 500 Index is up 14.8%, driven by large-cap technology stocks and telecommunication companies benefiting from AI capital spending. For the third quarter of 2025, the broad market index rose 8.1%. While tariffs have dominated the policy headlines under the new administration, the stock market has consistently rallied on news that tariffs will not be enacted to the degrees originally presented. Put simply, avoiding the worst-case tariff outcomes has been applauded.

The on-again, off-again tariffs have, however, weighed on the US economy. Reconfiguring the US supply chain will not happen overnight, and businesses are hesitant to upend operations with uncertainty over the lasting nature of any tariffs. Food prices are creeping higher, and job growth has stalled. Strain on the labor market has been building, and various data series have confirmed signs of stress.

In response to the changes in the labor market, in September 2025, the Federal Reserve lowered the short-term interbank lending rate by 25 bps and signaled the likelihood of further rate cuts. After having battled pandemic-related inflation for several years, the Fed has determined that cracks in the labor market necessitate it shift its focus from inflation and to unwind the restrictive monetary environment in support of job growth. The task confronting the Federal Reserve is precarious as tariff-induced inflation remains a real risk. Threading the needle to support employment, while avoiding stagflation (rising prices and unemployment) will be difficult.

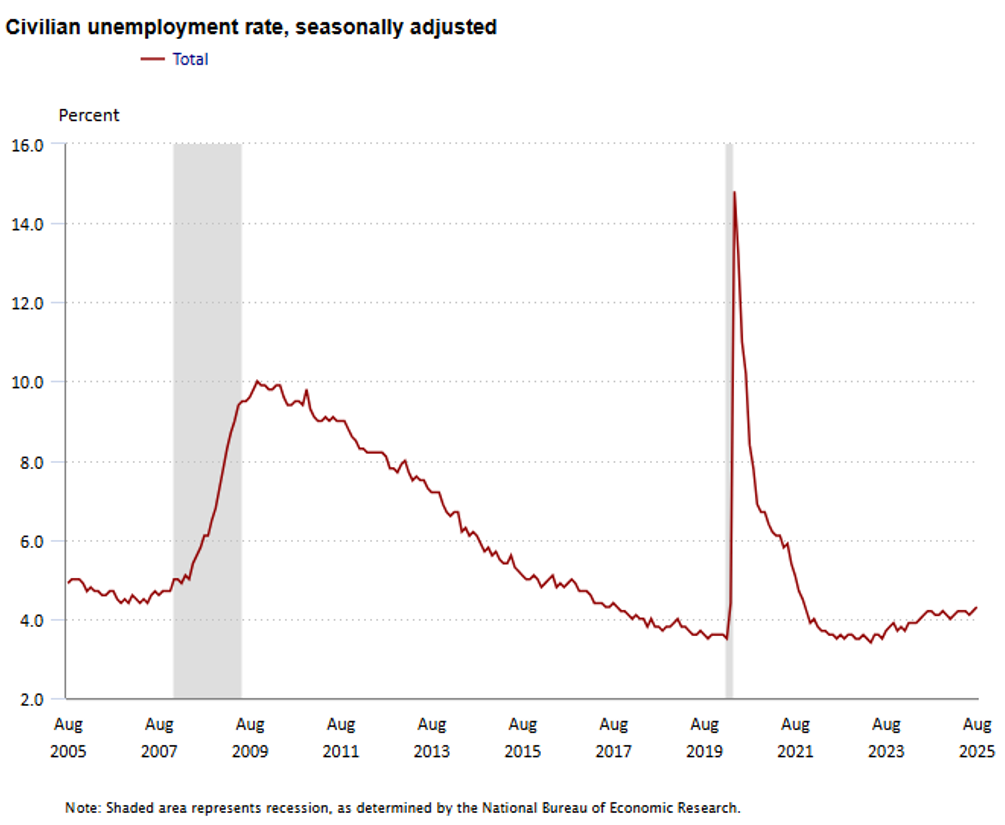

The chart above shows the slow climb in the civilian unemployment rate from a low of 3.4% in April 2024 to 4.3 % in August 2025 and underscores the Fed’s shift to thwart its progression. Private employment data, as seen by the ADP Report, has also fallen three of the last four months, showing job losses and revisions indicating a bleaker assessment.

Federal Reserve Chairman Powell has proven to prefer a slow and methodical approach to changes in interest rate policy. We expect this easing cycle to be no different, despite mounting pressure from the Trump administration, at least for now. Further interest rate reductions are likely, but the pace of the decrease will depend upon whether the employment data deteriorates further. Complicating the employment situation is a series of revisions to data questioning the veracity of the underlying job market. Just last month, the Bureau of Labor Statistics revised 2024 job growth significantly, raising further concerns about the reliability of recent economic strength and weaker-than-expected job strength. Certainly, the ambiguity around government spending, immigration raids, DOGE firings, and trade policy only add to the cloudy employment picture.

Thus far, US stocks continue to tolerate tariff sand being sprinkled into the gears of economic activity. Market participants have become indifferent to the trade war threats, policy reversals, or uncertain legality of the import duties. With the administration’s tariff policy initially being ruled unconstitutional through its use of the International Emergency Economic Powers Act (IEEPA), it appears the worst-case, or more destructive consequences, might be avoided. The US Supreme Court is set to address the IEEPA issue in the near future, but even if the current tariff policy approach is curtailed, Congress and the Administration have other paths that achieve similar effects.

Ultimately, only time will tell whether the decoupling from the global economy has lasting implications, or if the taxation that tariffs produce will dump too much sand in the economic engine of the US economy. A tariff is a tax on domestic businesses that will either suffer lower margins or push higher prices onto consumers. Tariffs have the secondary effect of acting as a brake on overall economic activity. Any slowdown in economic velocity will create a drag on employment. But until companies start reporting lower growth, falling margins, or inflation becomes more persistent, the frenzy around AI will remain. Thus far, however, the current record high level of overall earnings (EPS) and profit margins is among the strongest evidence validating US stocks position at all-time highs.

As of the writing of his commentary, Congress has been unable to agree on funding the government, and a shutdown is underway. Equities prices don’t seem too concerned, but this could change. For now, the default assumption is that both sides will need to compromise in order to keep the government open or that any closure will be temporary. Prior government shutdowns, while inconvenient, had been largely ignored by long-term investors.

Regardless of what happens in Washington, the market’s focus on AI and the potential economic benefits continue to drive the large-cap technology companies. Given the outsized weight these stocks maintain in the market-cap weighted indexes, such as the S&P 500 and Nasdaq 100 indexes, their performance is carrying the market. This cohort of large, highly profitable technology leaders are able to invest aggressively, independent of debt markets, and use their competitive advantages to solidify future opportunities. It is an enviable approach.

At some point, the divergence between the US equity market and the economy will reconverge. But predicting the timing of any reversion is difficult. Afterall, stocks tend to be forward looking, while economic data is by nature backward looking. With the economic benefits that AI might beckon and a more accommodative monetary policy forthcoming, it appears US stocks have so far tolerated less favorable economic data, though it is unclear how long the dynamic will persist.

Thanks for investing with Oak Associates.

Kind Regards,

Robert Stimpson, CFA

Chief Investment Officer

Oak Associates, ltd.

Grow stronger together.

The investments referenced in this article may or may not align with those currently recommended or held by Oak Associates for itself, its associated persons, or on behalf of clients within the firm’s strategies as of the date indicated. These investments are subject to change. The mentioned investments do not necessarily represent all those bought, sold, or recommended to advisory clients over the past twelve months. Portfolios in other Oak Associates strategies may contain the same or different investments, due to factors such as varying investment strategies, client-specific restrictions, mandates, substitutions, liquidity requirements, or legacy holdings, among others. The investments highlighted were not selected based on their past performance. Readers should not assume these investments have been or will be profitable in the future.

Past performance is not a reliable indicator of future results. Investments can lose value, and there is no guarantee that any strategy or product will achieve its objectives or perform as anticipated. All investments involve risk, including the potential loss of principal. Before making any investment decisions, individuals should assess their risk tolerance and seek advice from a financial advisor. Information that is sourced from a third-party is assumed to be accurate but is not guaranteed. This commentary does not constitute an offer or solicitation to buy or sell any financial products.

The S&P 500 Index is a well-known, market-capitalization-weighted index of 500 widely held U.S. equities, designed to reflect broad U.S. stock market performance.

CFA is a registered trademark of the CFA Institute.