2024 Third Quarter Market Commentary

Commentary

Nearly Out of Patience

All year, investors have been eagerly awaiting Federal Reserve action to remove the significant tightening it imposed following the Covid-19 Pandemic and resultant inflation. While Wall Street believed sufficient evidence existed to lower interest rates long ago, in lieu of decisive evidence that inflation busting measures were causing a recession, Chairman Powell opted to preserve the restrictive monetary environment.

Yet, when the Fed announced its decision to remain firm at the July meeting, US equities threw a temper tantrum. The S&P 500 fell 6% in the first week of August before spending the rest of the quarter reclaiming all lost ground.

With the market’s annoyance well noted, the Fed did act to lower short-term interest rates by a full 50 basis points at its mid-September meeting. By the end of the third quarter, the S&P 500 had risen 5.8% for the quarter and 22% YTD. We have long commented that the market’s expectation for a rapid reduction in tight monetary conditions imposed was overly optimistic, especially without definitive evidence of problems in the labor market or rising recession risk. Lacking these, the Fed would remain reluctant to lower rates despite investors’ preferences and the consensus expectations for multiple rate cuts earlier this year. What we did not expect, however, was the outsized 50 bps decrease as the Fed’s first action to unwind the restrictive rate environment.

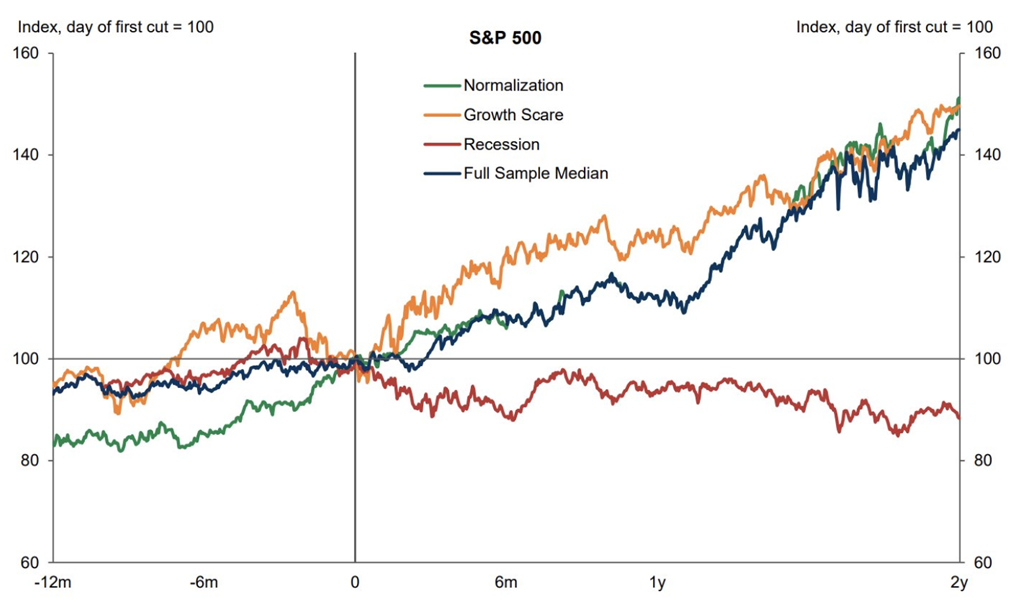

Historically, outsized rate cuts have coincided with Fed intervention to address an unfolding economic crisis. We do not believe that is the situation today. Normally, with rate cuts, slow and steady wins the race. Instances where the Fed is simply normalizing the interest rate environment, stocks tend to perform well 6-, 12-, 18 months out. When steep rate cuts are required in response to a crisis, forward market returns are generally lower. As shown in the chart below, the character of the Fed’s interest rate cycle is important.

Equities have tended to rally further after the first Fed cut when easing is driven by modern policy normalization

Median across each sample

(1928 – 2021)

Source: Goldman Sachs Global Investment Research

Regardless of the glide path the Fed takes to reduce its prior interest rate increases, we continue to expect rates to remain “higher-for-longer”, relative to historical levels. We do not anticipate a drop to sub-3% short-term rates, even though there are some Wall Street economists forecasting a return to the pre-Covid levels. Given the economy’s recent inflation problems, we expect rates to return to a neutral level, but not beyond to a stimulative level. We also recognize the Fed’s desire to retain the power of rate cuts should a future crisis arise. With one of the strongest global economies currently, there is no need to risk reviving inflation or removing slack in the labor market.

The sector participation behind the broad market indexes has been interesting this year. The strength in Technology and Telecommunication stocks has been well documented due to the hype surrounding Artificial Intelligent (AI). Yet, rate sensitive sectors, such as Utilities and Financials, have both been strong. Within the consumer sectors, more defensive staples are actually outperforming discretionary stocks. Meanwhile, the commodity-related sectors, Energy and Materials have been lagging the S&P 500. Their underperformance while the Fed was suppressing inflation is expected, but lower rates and a recent rebound in oil prices could help. Overall, markets that show wide participation tend to be healthier and more representative of broader economic strength.

The past three months have seen the U.S. stock market navigate a period of heightened volatility, largely shaped by interest rate policy and inflation concerns, but also rising geopolitical risk. The Middle East, often a hot spot, can affect energy prices, which in turn impacts global economic activity. Such events can cause short-term weakness, which then subsides once investors discount the global economic implications. Using the Ukraine-Russia conflict as a recent example, US stocks suffered in the two months following the onset of hostilities in February 2022. Since then, however, the S&P 500 has risen 37% despite the ongoing war. We will continue to monitor the situation in the Middle East.

In summary, the U.S. stock market benefits from the Federal Reserve finally initiating the cycle to unwind its restrictive monetary conditions. The stock market will continue to navigate competing risks of recession fears, renewed inflation and geopolitical turmoil. Yet, despite these challenges the life that lower rates will breathe into the housing sector, consumer credit and sentiment is extremely beneficial. The US consumer remains the driver of economic activity and constraints on auto financing, mortgage affordability and consumer credit can reverberate through the economy.

Thank you for your investment with Oak Associates.

Robert Stimpson, CFA

Chief Investment Officer

Oak Associates, ltd.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell. This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization-weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.