2023 Third Quarter Market Commentary: Standing Tough

Commentary

2023 Third Quarter Market Commentary

Standing Tough

The S&P 500 fell 3.27% in the third quarter of 2023. Despite the decline, the broad-based US market index is up 13% year-to-date. Overall, both the economy and the stock market are standing tough despite the rapid rise in interest rates over the past 18 months. The resilient job market and tapering of the Federal Reserve’s interest rate tightening cycle have sustained market gains. And while normally maligned for its maneuverings, the Fed deserves recognition for manufacturing an attack on inflation without rocking employment.

For most of 2023, a recovery in growth-oriented sectors, hope that the economy would indeed avoid a sharp recession, and optimism over the end of the Fed’s tightening cycle has buoyed the market. The surge in artificial intelligence (AI) focused stocks and hype surrounding the sector has certainly helped some areas of technology. In Q3, however, the AI frenzy subsided and more traditional economic factors weighed on equities, specifically higher energy prices, rising bond yields, and US dollar strength. Semiconductor stocks, which supply the engine parts of AI innovation, fell nearly 7% in the third quarter, but remain up 35% this year (as seen by the Philadelphia Semiconductor Index). West Texas Intermediate (WTI) Oil rose 35% in the quarter as dollar strength and global supply cuts fueled a sharp rally. We remain skeptical of sustained energy strength given global economic conditions.

Investors and economists alike generally view the Federal Reserve with perpetual skepticism. History is littered with examples considered policy mistakes. The Fed is apt to either overtighten interest rates, allow a “lower-for-longer” rate environment to fuel excesses that ultimately threaten markets, delay action too cautiously, or preempt economic expansions prematurely. It was criticized for failing to act decisively in the leadup to both the dot-com era and the subprime crisis. In more recent history, its prolonged zero interest rate policy (ZIRP) following the ebb of the Coronavirus pandemic helped to foster inflation. Everyone’s a critic (including us) and hindsight is 20/20.

As active market participants, our default expectation is that the Fed is essentially behind the curve in addressing structural economic issues and will overdo its attempts to unravel problems. It is a very fine balancing act to manage the economy, promote employment, avoid inflation, and solve crises as they appear. We generally expect that any backward-looking, slow-moving government bureaucracy is at a significant disadvantage in the face of complex issues. That said, the Federal Reserve deserves credit for successfully suppressing inflation over the past 2 years, protecting the strong job market, and supporting the economy, all while faced with the risk of a regional banking crisis. The net result of this has been a decent stock market in 2023.

Our knowledge of market history and the Fed’s previous mistakes keeps us vigilant that the next misstep is always possible. The last time the Fed addressed a serious inflation problem in the 1970s, it struggled until aggressive and decisive action from Chairman Volker turned the tide. Chairman Powell may have deserved criticism for being late to the inflation fight, but he has calmly and methodically made significant progress.

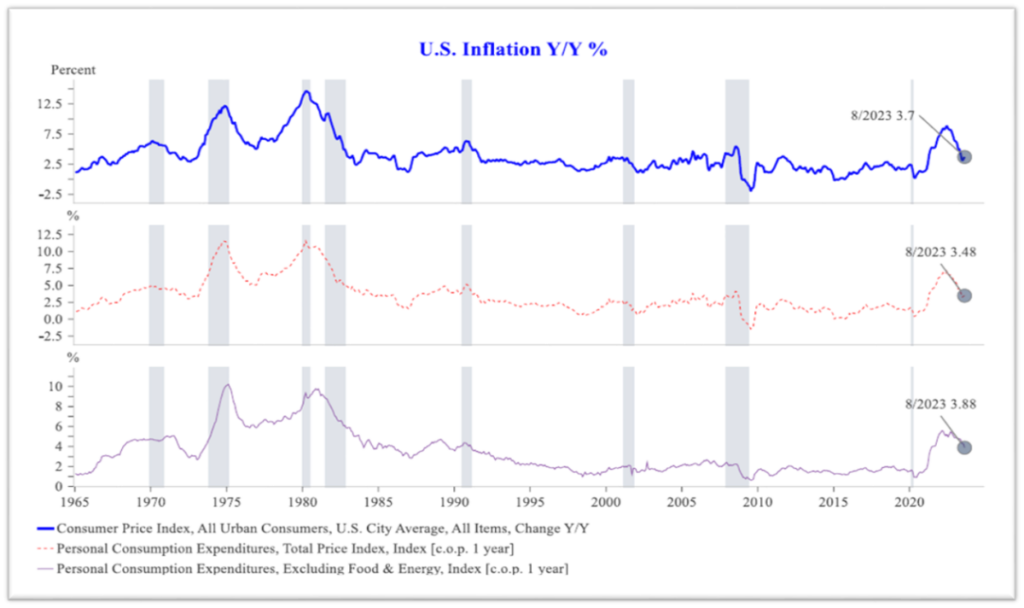

The chart below shows that regardless of your preferred measure of inflation; the consumer price index (CPI), with or without food or energy, etc., the reduction in inflation is clear. We are not naive enough to declare victory but acknowledge credit where credit is due.

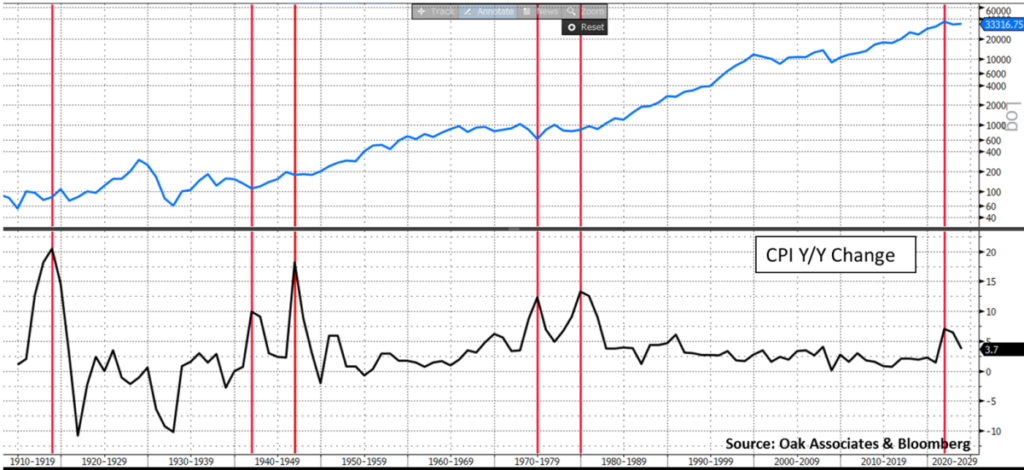

For equity investors, the following chart should be reassuring. While the stock market’s long-term upward bias is well documented, periods of inflation damage this tendency. More important, however, is the success the market achieves once the inflation problem has dissipated. Stocks simply perform better when inflation is constrained. The market’s gyrations and corresponding turning points are lost in this 100+-year chart, yet our point is that victory over inflation is a major long-term positive for forward equity returns and preserving the market’s upward bias.

Dow Jones Industrial Average 1914 – 2023 (logarithmic)

Going forward, the next step in the Federal Reserve’s interest rate glide path remains uncertain. Debate persists as to when it will unwind the substantial tightening imposed, or if a few more rate hikes are needed to prevent an inflation resurgence given higher energy prices recently. This is understandable. Even we remain concerned that the sharp changes early in the tightening cycle are still working their way through the economy and could initiate an earnings decline. Yet, the talk of a soft-landing, hard landing, no-landing, rolling recession, etc. has dominated the financial media for 2 years now. We will certainly have a recession at some point, but the chatter tends to overlook the fact that the driving force behind the economy, the spend-happy consumer, remains confident, gainfully employed, and is less worried about inflation. The combined power of a healthy consumer and job market is helping the economy and the stock market to defy recession prognosticators.

As we enter the fourth quarter, stocks tend to demonstrate seasonal strength, particularly when consumer confidence is high heading into the holiday shopping season. With interest rates now reset to higher levels, the Fed’s tool kit is also rearmed. In prior commentaries, we had discussed how low-interest rates handicap the Fed’s ability to manage economic risk. Reclaiming the powerful interest-rate arsenal is an underreported positive. Higher yields, a slower housing market, and steeper mortgages are all brakes on economic activity to monitor. Yet for now, the economy, and the Fed, are standing tough despite the naysayers.

Robert Stimpson, CFA

Co-Chief Investment Officer

Oak Associates, ltd.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell. This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization-weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.