2023 Second Quarter Market Commentary: Fed Stays Hawkish

Commentary

2023 Second Quarter Market Commentary

Fed Stays Hawkish

Our message this year has remained unchanged believing that the first half had the potential to be better than the second (2023 Outlook). After falling nearly 20% in 2022, US markets have bounced off October lows to return over 16% thus far in 2023. Despite a banking crisis in the first quarter and a debt ceiling quandary more recently, equity prices have continued to grind higher. Given the lagged effect of monetary policy, however, the lion’s share of the current tightening cycle is likely to be a significant second-half headwind and Chairman Powell has made clear the job is still not done. As a result, we expect volatility to persist until the Fed pivots to rate cuts or at least declares victory in its fight against inflation.

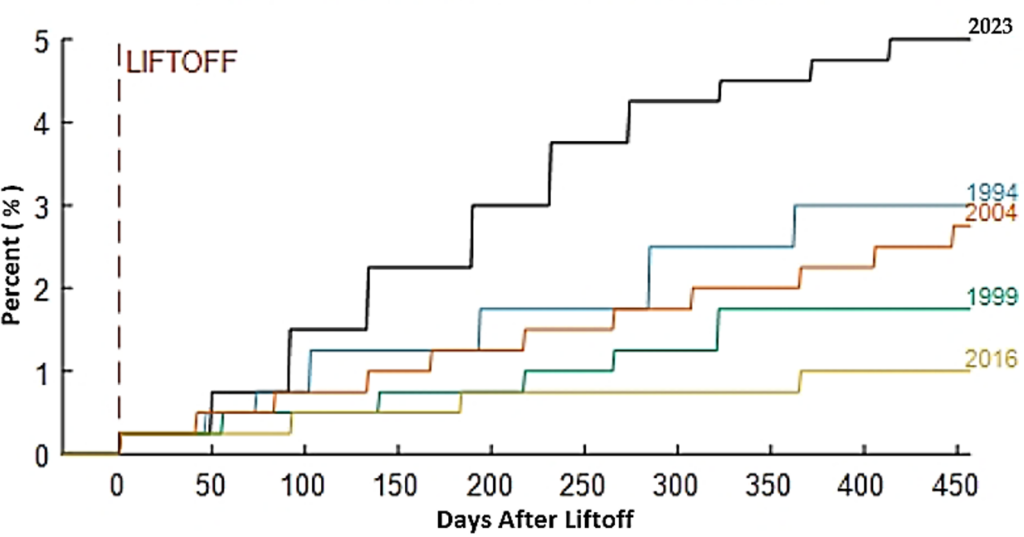

The Federal Reserve has carried out an aggressive pace during its current tightening campaign by lifting interest rates from zero to 5% in just over a year, as can be seen in the chart below. Despite the rapid and significant increase, there is much debate as to whether policymakers have already gone too far or still have not gone far enough. Most economists agree that changes in Fed policy in either direction can take at least a year if not longer to work their way into the economy. With this in mind, it is important to remember that the bulk, 70%, of the total increase in interest rates, occurred after June 30th, 2022.

Fed Tightening Cycles: TARGET INCREASES

Source: Piper Sandler

The actions of the Fed are having the desired effects. The economy has slowed as has the pace of price increases (CPI chart below). And while inflation has not yet returned to the targeted 2% level, we believe current economic data suggests it will remain on its downward path in the quarters to come. Tighter lending standards since the bank failures earlier this year, as well as persistent weakness in leading indicators, suggest that economic growth will continue to moderate from here.

Source: Bloomberg

In spite of the turbulence and uncertainty, US markets have made impressive gains so far this year. Due, in part, to a bounce off correction lows when investors had anticipated a more rapid and substantial economic deceleration. Instead, while economic growth has slowed, it is still positive and growing at a 1-2% clip. Further, inflation is moving in the right direction and the consumer has remained healthy. Cooling inflation and a resilient consumer have increased hopes for a best-case or soft-landing scenario (i.e. no recession) which has allowed markets to maintain their upward trajectory.

The data set we are monitoring most closely remains the labor market. A significant part of the Fed’s plan to bring down inflation is to create slack in employment in order to ease upward pressure on wages. Conversely, the pandemic has created some lasting impact on the overall labor supply, as workers have been slow to return for a variety of reasons ranging from permanent retirement in the case of aging baby boomers, to inability from lasting health issues both of which have made the Fed’s job more difficult. Thus far, the rate of wage growth has been slower to moderate than that of prices and remains elevated.

Financial pundits have been calling for a recession ever since monetary policy began tightening a little over a year ago. Nevertheless, the economy and markets have stubbornly resisted. The accumulated tightening still in the pipeline, combined with Chairman Powell’s directive that there is still more to come lead us to our opinion that volatility will endure in the near term. That said, for those willing to look beyond the next six to twelve months, we believe there is cause for optimism. Although rates have risen, they remain relatively low and certainly in a range that can support growth. Further, consumers have seen wages rise in recent years which bodes well for our consumer-led economy longer term.

Once markets feel confident inflation has been tamed, we anticipate that a focus on high-quality, profitable growth companies will be a key characteristic to outperformance. The investment backdrop has evolved with the increase in the cost of capital. Due to the elimination of zero-percent interest rates and the proverbial free lunch for those seeking new capital, stock selection is likely to once again be an essential component of successful investment returns.

As always, thank you for reading and please do not hesitate to reach out to us if we can assist you with achieving your investment goals in any way.

Kindest Regards,

Jeff Travis, CFA

Portfolio Manager and Senior Analyst

Oak Associates, ltd.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell. This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization-weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.