2023 First Quarter Market Commentary: Unexpected, But Not Totally Unexpected

Commentary

2023 First Quarter Market Commentary

Unexpected, But Not Totally Unexpected

In the first quarter of 2023, US stocks were rattled by a series of banking crises. While the events were unsettling, decisive actions by the Federal Deposit Insurance Corp (FDIC) seem to have preempted a wider contagion. Despite a pair of the largest bank failures by assets in US history, the S&P 500 still rose 7.48% during the first quarter. Nevertheless, repercussions of the abrupt financial crisis will likely increase the risk of a recession while simultaneously propagating the end of the Fed’s tightening cycle and inflationary pressures.

The succession of banking crises was both expected and unexpected at the same time. Per se, the initial demise of Silvergate Capital was not surprising given its exposure to cryptocurrencies and the FTX collapse. Nor was the Swiss government’s facilitated rescue of Credit Suisse. The distinguished European banking giant had fallen 90% over the past two years after a series of scandals damaged the bank’s reputation. However, the abrupt collapse of Silicon Valley Bank (SVB) in early March was not widely predicted and its rapid implosion reverberated throughout the financial system. As of the end of the quarter, the fate of several other regional banks remains indeterminate.

In essence, Silicon Valley Bank succumbed to a 21st-century bank run, where customers sought to electronically withdraw a substantial percentage of the bank’s deposits in a very short period. In a fractionally banking system, the inability to satisfy redemption requests and the massive decline of its capital base necessitated the intervention and seizure by Federal regulators. SVB was integral to the banking of start-ups and financing by venture capital firms in California. Ironically, it was private equity and Venture Capital firms that instigated the bank run by advising their portfolio companies to divert funds away from SVB once questions over the bank’s losses and capital arose. That is not to say these entities are to blame for the collapse of SVB. Indeed, an incredulous absence of interest rate risk hedging, poor internal controls, losses on supposedly safe long-term held-to-maturity securities, a mismanaged capital raise, and a reliance on early-stage companies all played a part in the bank’s failure. The toppling dominos ultimately culminated in the FDIC seizure and its unprecedented decision to insure all deposits at the bank.

Irrespective of the moral hazard risk argument this creates, the one surefire way to avoid another bank run is to make all depositors, regardless of location or amount, believe that their money is safe and can remain at their corner bank. On the heels of the SVB collapse, the FDIC also closed troubled Signature Bank in New York and insured its depositors as well. Additional liquidity has also been provided to other regional banks to prevent issues similar to those at Silicon Valley Bank.

Oak Associates did not own any Silicon Valley Bank, Signature Bank, Credit Suisse, or Silvergate Capital. In regard to financial stocks, our preference has always tilted toward larger, more diversified companies.

When the house next door burns down unexpectedly, you can bet that all the other neighbors make sure their homeowners’ insurance is up-to-date and includes fire protection. Similarly, the problems at SVB and Signature Bank are likely to propel other regional and mid-sized banks to review their interest-rate hedging, capital reserves, and risk controls. The neighborhood will now be collectively safer. This may not make regional banks a sound investment, however. In order to dissuade clients from fleeing for higher returns in money market funds or fixed-income products, banks will need to offer more competitive deposit rates. This will hurt earnings power and margins in the sector.

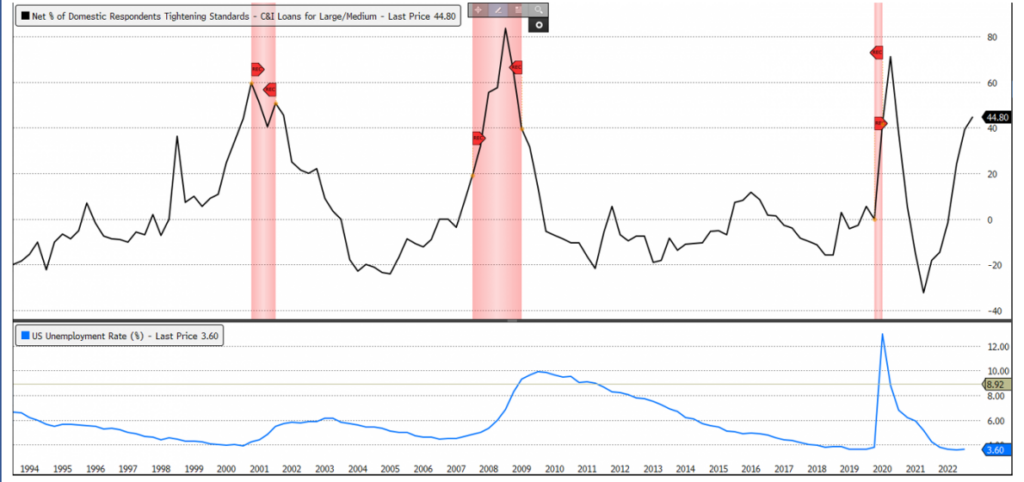

In addition to efforts to retain deposits, banks are raising lending standards due to concerns over the economy and extending fewer loans. Not only will this also hamper earnings, but it will add braking pressure to the broader economy by decreasing the velocity of money. Tighter lending standards tend to occur around recessions and often lead to an increase in unemployment.

Lending Standards vs. US Unemployment w/Recessions

Source: Bloomberg, The Federal Reserve

In late March, despite previously hinting that a 50-basis point (bps) interest rate hike might be in contention, the Federal Reserve enacted a smaller 25bps increase in light of the regional banking crisis. This matched our expectations. While the Fed is responsible for regulating financial institutions, its primary mandates are inflation and employment. With the Consumer Price Index (CPI) still well above a 2% target level, the Fed’s smaller interest rate hike acknowledges the financial contagion risk without retreating from the battle against inflation. The smaller rate hike has fueled optimism that an end to the tightening cycle is near, but in practice, the stricter lending standards may prove to be more of an economic impediment than the 25 bps.

The Federal Reserve’s and FDIC’s actions do appear to have curtailed the unfolding financial crisis, but the severity of the interest rate increases since March 2022 were unquestionably a major factor in the recent crisis. Things bend until they break. The massive increase in the Fed Funds rate from 0% to 4.75% over the past 12 months, combined with the diminishing benefit of inflation on revenues, is precisely why we anticipate that corporate earnings may falter later this year. We continue to favor high-quality investments with a tilt towards profitable technology companies and the stable healthcare sector. Higher interest rates, and tighter lending standards, have a pronounced detrimental effect on companies that rely on debt financing and on the spending for goods that require financing. While the decelerating velocity of money will help in the battle to thwart inflation, as an equity investor, pressure on earnings is never beneficial.

Finally, although the immediate risk of a financial contagion may have been averted, the next predicament will be Congress’s forthcoming argument over the debt ceiling. See our recent article on the debt ceiling here. While the stock market is arguably apolitical (based on return attribution), investors are not immune to uncertainty. The prospects of a US default, even if temporary or more logistical, could rattle markets. We continue to monitor the situation.

Robert Stimpson, CFA

Co-Chief Investment Officer

Oak Associates, ltd.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell. This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization-weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.