2020 First Quarter Market Commentary: Intellectually Honest

Commentary

Intellectually Honest

The first quarter of 2020 was a difficult period for global equities. The Covid-19 pandemic overwhelmed global markets as fear, uncertainty, and a sharp reduction in economic activity combined to send many asset classes plummeting. The S&P 500 lost 20% in the first quarter with most of the damage coming in just three consecutive weeks.

Global public health agencies have determined that the best course of action to fight the Coronavirus is to essentially impose social distancing restrictions to limit the transmission rate of the disease. This should help maintain hospitals’ ability to care for the affected without overwhelming the health care system. The byproduct of this strategy, however, is a sustained suppression of economic activity. Workers are confined to home, businesses are closed, and stay-at-home orders are in effect. While many market participants predict a quick return to normalcy, these forecasts may prove optimistic. Calling a market turn is usually foolish and forging a bottom tends to be a process that occurs over time.

In our year-end 2019 market commentary, Monsters Under the Bed, we discussed the two items that could possibly end the 11-year bull market. At that time, higher interest rates were a risk as it appeared the Federal Reserve (the “Fed”) sought to rearm its toolkit in preparation for the next recession. It never quite reached full rearmament and instead has had to cut interest rates to zero in response to the unprecedented health care crisis.

The second concern was a shift in employment trends. When unemployment increases, it has reverberations across the economy as it affects not only income levels, but consumer spending, loan delinquency rates, home sales, auto sales, consumer confidence and more. It is this increase in unemployment and its lingering effect on the economy we feel may be underappreciated by market participants hoping for a V-shaped recovery.

In the fourth quarter of 2019, the stock market experienced a similar sharp drop, collapsing 20% intra-quarter on concerns over the Fed’s posturing. However, the stock market quickly recovered, because the decline was not driven by underlying economic data. Unfortunately, the Q1 2020 decline corresponds to a significant change in unemployment, an important economic indicator. It would be intellectually dishonest of us to ignore a pending jump in unemployment.

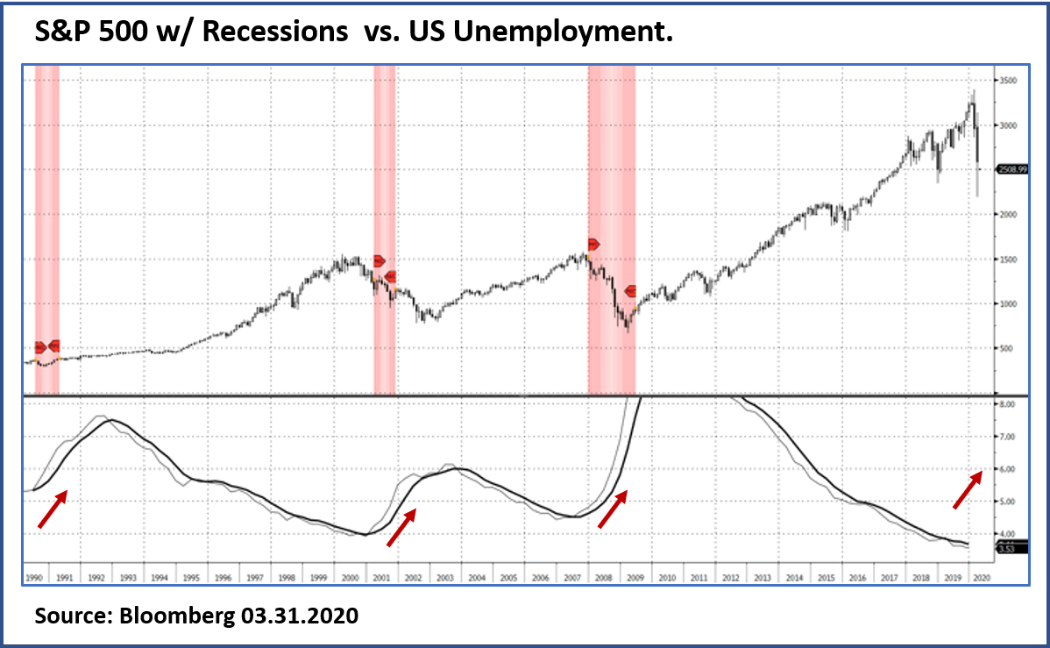

In the chart below, the top half of the chart shows periods of recession while the bottom half shows trending US unemployment.

The number of US workers seeking unemployment benefits skyrocketed this March 2020 as businesses had to lay off staff while their operations were shuttered. Weekly jobless claims, a key leading indicator for the national US unemployment rate, had been around 250k but surged to 6.6 million almost overnight. The prospects of economic devastation for small businesses and those affected by the “shelter-in-place” pandemic strategy caused Washington to enact a large, broad, $2 trillion stimulus package with support for businesses affected by the Coronavirus, which also includes a direct payment to all US citizens earning less than $95,000 per year. While Congress acted swiftly to agree on a stimulus package, the lessons from previous crises suggest that multiple attempts are usually needed to address the underlying problem.

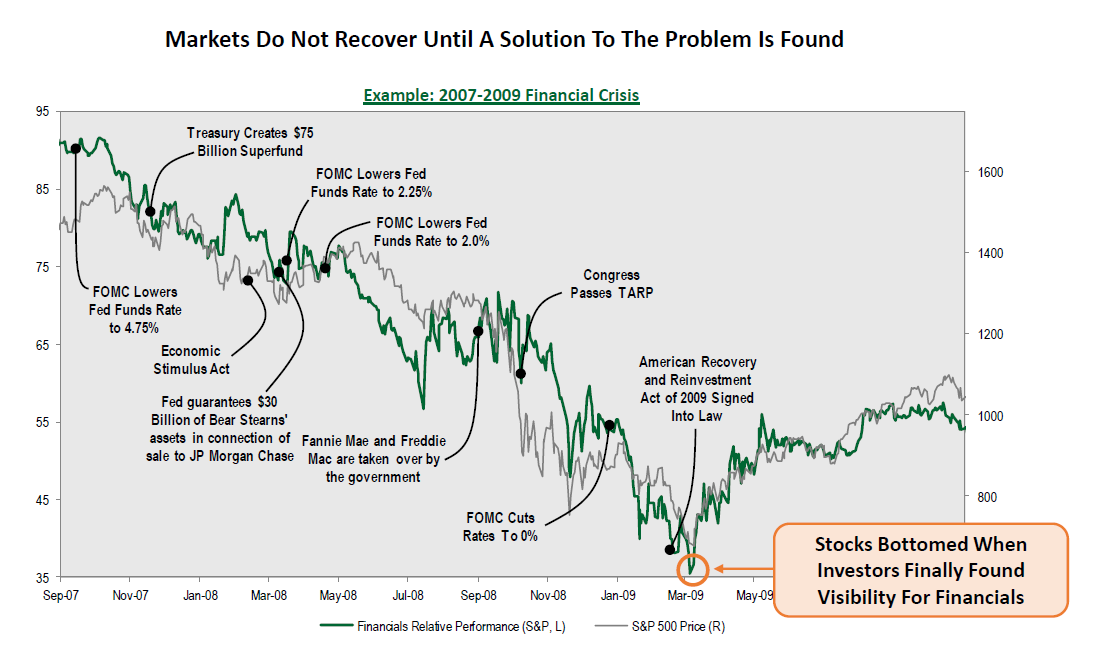

The chart below from Cornerstone Macro details the performance of Financials during the 2008-2009 sub-prime crisis. It notes the nearly dozen governmental actions taken to solve the crisis before stocks were able to find a bottom. While the market has responded positively to the recent stimulus package, the economic pain may not yet be fully understood and further supportive actions may be required. The US stock market may therefore struggle to return to pre-Covid levels while still facing months of terrible earnings report, the realities of the economic destruction caused by the pandemic, and potential flare-ups of the virus once quarantines are loosened. Unlike prior stock market corrections, this one is not driven by a fragility within the financial system, but by an unprecedented health care crisis.

The unique nature of this market cycle has prompted Oak to shift exposure within our portfolios. Put simply, the situation on the ground has changed. The investment landscape and its environment are different going forward. We are also seeing numerous attractive opportunities given indiscriminate selling when the pandemic broke. We have therefore reduced our exposure to areas whose earnings prefer higher net interest margins and healthy lending. We are also expanding into other sectors with strong secular growth drivers which may benefit from the targeted stimulus package. Our investment process already leads us to market-leading companies with strong balance sheets, and relative performance during this crisis has been solid.

History indicates this crisis will pass and the stock market will recover. If anything, this market correction feels more like the dot-com bubble than the sub-prime crisis. While all market cycles are unique, the sharp reduction in capital spending that occurred after Y2K and the resulting recession are more comparable to the current rapid decrease in economic activity. We continue to monitor our portfolios and remain vigilant for attractive opportunities.

Thank you for reading.

Robert Stimpson, CFA, CMT

Jeff Travis, CFA

Portfolio Manager

Mario Montoya

Research Analyst

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell.

To determine if this Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund’s Prospectus which may be obtained by calling 1-888-462-5386 or visiting our website at www.oakfunds.com. Please read it carefully before investing.o determine if this Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund’s Prospectus which may be obtained by calling 1-888-462-5386 or visiting our website at www.oakfunds.com. Please read it carefully before investing. Mutual fund investing involves risk, including possible loss of principal.

Mutual fund investing involves risk, including possible loss of principal.

This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC. Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.