Seeing Through The Trees

Insights

Clearing emotion to stay on track with the long-term investment goal.

We are all emotional beings and investing takes us through an unnatural journey of psychological twists and turns. We set aside investment capital for that journey of delayed gratification to reach a desired long-term goal (future reward).

Along the way, we experience a number of natural emotions that can lead to counterproductive actions in our pursuit of that desired outcome, such as: a heightened sensitivity to short-term losses over big picture gains, seeking reassurance by waiting for a positive move before investing, the belief that we can increase performance by timing the market, and the fear of missing out on a running investment trend. These are natural emotions that generally lead to poorly timed investment decisions. However, there are ways we can mitigate such emotions, the trees blocking our view to the long-term investment goal.

The Financial Advisor Effect

A financial advisor can be a key sounding board providing guidance and setting up a long-term financial plan. An advisor is there to bring an understanding of behavioral finance and to help mitigate potential counterproductive, emotion-driven decisions. Advisors assist with maintaining a long-term perspective and an objective eye on diversification, while also coordinating properly timed rebalancing efforts. When working with a financial advisor, you have someone who knows your full family picture including all accounts, insurances, retirement goals and inheritance plans. They can also assist you with strategic tax loss harvesting and determine which investment accounts to trade to optimize when gains/losses should be realized or instead pushed into later years. The financial advisor can help avoid a potential panic sale where an investor is looking at one aspect of their portfolio but where that advisor may have built in other investments that counteract or diversify away some of that risk. Along the way, the advisor can ease an emotional reaction to a loss by explaining where it may end up being a benefit in unexpected ways, such as at tax time or as part of a coordinated strategic shift.

At Oak Associates Funds, we recognize the important role played by our network of financial advisor partners and have built our dual-concentrated, fully invested equity growth investment process to also fit within broader customized investment plans. By staying fully invested in our portfolios, we allow the excess short-term cash decisions to be made at the financial advisor/client level, since each client has unique needs and variable investment path timing. This helps make allocation planning more deliberate and transparent.

Use Time to Your Advantage and Stay Invested

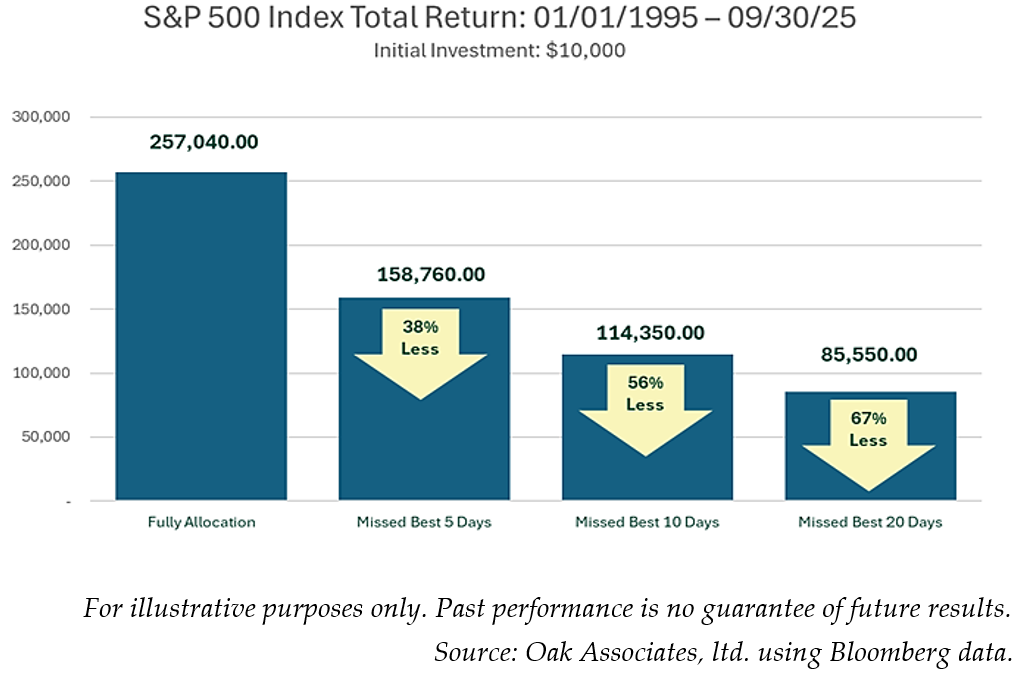

The value of an investment is a culmination of three variables: amount invested, time invested and rate of return. We have the most control over the first two in achieving the optimal benefits of compounding. Investing early and staying invested has been a hallmark of building wealth through compounding interest. The urge to time markets, where timing decisions must be correct twice, or to chase winners, where often a decisive move has already been missed, most often leads to less optimal outcomes versus simply sticking to a well-planned long-term allocation. We are reminded again of the risk that comes with timing the market by the latest DALBAR Quantitative Analysis of Investor Behavior report release, indicating: “Despite strong performance in the equity markets, investors continued to underperform due to their behavior. Withdrawals from equity funds occurred in every quarter of 2024, with the largest outflows taking place just before a major surge.”1 The potential impact of a poor market-timing decision is further illustrated in the graph showing how just missing a few of the best days, using the S&P 500 Index© as an example, could have a long-term impact on an investment.

Don’t Underestimate the Power of Automatic Investment Plans

It is not always possible to front-load your investment and that’s where an automatic investment plan and the related dollar-cost averaging effect should not be underestimated. An automatic investment plan can be an effective investment tool in maintaining a disciplined investment process, while also potentially limiting emotional decisions. Knowing that a fixed dollar amount will automatically be invested on a scheduled basis can minimize our temptation to jump in and out of the market. In essence, why would I make an emotional sale when I’m scheduled to buy more of it right back? I can set an amount on a fixed schedule and let the dollar-cost averaging impact help smooth out market fluctuations over time, taking advantage of the fact that more shares are bought during times of lower prices than at times of higher prices. This can lower the average cost per share and help to quell the fear of buying at the wrong time (failure to launch while waiting for an unknowable perfect time to buy), or the emotional tendency to sell low (during market turmoil), or fear-of-missing-out urge to buy high (during market exuberance). Finally, for those investors that knowingly just wish to be more individually active within the markets, setting an automatic investment plan at the core of an allocation may at least partially lessen the overall potential impact by limiting such movements to smaller amounts at the margin.

At Oak Associates, we believe that sustainable long-term growth for investors is best achieved through a concentrated focus on companies and sectors. Accordingly, we maintain this Dual-Concentrated Investment Approach when managing the Oak Associates Funds. I hope you find value in these thoughts and thank you for your time.

1 “Investors Missed the Best of 2024’s Market Gains, Latest DALBAR Investor Behavior Report Finds”, Dalbar, March 31, 2025.

For more mutual fund information, call today: 1-888-462-5386 or visit our website at www.oakfunds.com

Should any financial advisors have questions or wish further information, please contact Sarah Hill, our Director of Distribution & Advisor Relations, at [email protected]

Past performance is no guarantee of future results. Oak Associates Funds are available to U.S. investors only. The thoughts and opinions expressed in the article are solely those of the author as of October 15, 2025. The referenced indices are for illustrative general market comparisons only and not meant to represent performance of any fund. Investors cannot invest directly in an index.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Funds’ prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

Mutual fund investing involves risk, including the possible loss of principal. Oak Associates Funds are distributed by Ultimus Fund Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

20251106-4962749

More News & Insights